[The Weekend Bulletin] Rebooting 2022 - Links Worth Revisiting

A collection of some of good articles worth re-reading.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

We close the year by revisiting some of the best articles (in my opinion) that we've read through the course of the last one year, as has been the tradition1.

Other than the division in to relevant topics, there is no order to the articles. Feel free to explore the way you deem fit.

Rather than being read over a weekend or a week, this one is meant to be consumed slowly, over time. The ideal way would be to just bookmark this issue and then return to it for a deep dive into a topic that you wish to learn more about.

Please Note: Taking a break next week and then traveling for work. The regular issues of 2023 will hit your inbox from January 21st onwards.

Investing Wisdom

Investor Interviews/Letters/Profiles

Ramesh Damani discusses his investment journey, hits, misses, as well as regrets with Vishal Khandelwal on the One Percent Show. Mr. Damani has interviewed many a stalwarts in his Wizards of Wallstreet show, and he is no less a stalwart than his guests (he is one of the subjects of the book Masterclass with Superinvestors). There are many insights in this one, but one that I loved most was how his father got him interested in to investing.

Rajiv Khanna (of the Dolly Khanna fame) was an entrepreneur and did not start investing until the age of 50. His late start however, did not stop him from converting ‘6 to 2000’ in nearly two decades (a CAGR of ~34%). This is a rare interview of a usually media-shy investor, and an equally interesting story.

Samit Vartak (Founding Partner and Chief Investment Officer of SageOne Investment Managers) talks about his humble beginnings, success vs happiness, Vedanta philosophy, living through the stress of a down year, and the joy and pain of managing other people’s money, on The One Percent Show

We've met him twice already in the not so distant past (#91 and #94). His story, however, is so inspiring that is worth listening to again. And so for the third time, please listen to Arnold Van Den Berg narrating his story and more on The One Percent Show.

This conversation with Guy Spier was so meditative. The most interesting part to me was the non-investment discussion around thank you notes and onwards. This one comes highly recommended: Guy Spier on Finding Your North Star and the Power of Compounding Goodwill - The One Percent Show

The latest (Fall 2022) issue of the Graham & Doddsville Newsletter from Columbia Business School carries three interesting investor interviews:

Jacob Rubin (Philosophy Capital) - search for mispricings, and differentiating between CFAR (cheap for a reason) and TCTI (too cheap to ignore).

Connor Haley (Alta Fox Capital Management) - Building an investment firm, activist investing, and learning from first principles.

Christopher Bloomstran (Semper Augustus) - Earning the Earnings Yield, Capital Bullets, and Aware Generalist. [highly recommended]

If investor letters were an episode, this one would be a couple of seasons. At 129 pages, it is the length of around half a book, and covers a multitude of topics (I am less than halfway through at the time of this writing). The first section of Christopher Bloomstran's (Semper Augustus) 2021 letter to clients talks about intrinsic value, and the link between earnings yields and forward returns. The second section charts the investments of two investors, a lesser known Mr. Smith and a well-known Mr. Buffett. The sections that follow cover thoughts on energy and commodities (oil), student-managed funds, book recommendations, followed by a deep dive into Berkshire. Lot of food for thought in this one.

William Green (author of Richer, Wiser, Happier) interviews Joel Greenblatt about concentration, margin of safety, magic formula, and more in this very insightful conversation. Below are two of my favorite moments from the conversation:

“And it's kind of like finding one of the best things you've ever seen, but putting one or two % of your portfolio into it. That's not getting it right. That's getting it wrong.”

“Yes, o, i think what you're alluding to is to be a really good investor and have a strong enough stomach, you have to have a screw loose some place to be able to handle it. And i think the answer is, yes, you have to have a little bit of a screw loose to be able to take those risks.”

The Legend of Li Lu - this biographical article traces the early life and journey of famed investor Li Lu towards investing. Not a lot of material is available on Li and that makes this well researched article even more prized. In case you didnt know, Li Lu's fund is one of the only three investments that Charlie Munger holds.

Robert Wilson falls under the title of “the greatest investor you’ve never heard of.” He turned $15,000 into $230 million from 1958 to 1986 - a stunning 41% CAGR. Wilson was a long/short investor who wasn’t afraid to use leverage. His is an interesting journey that culminates in to an important lessons for all investors - never let success go to your head. This articlediscusses one of his biggest losses, and also reproduces an interview that he gave towards the end of his career. (Interestingly, the interview also featured John Templeton and Warren Buffett. It's interesting how each of them had a different investment philosophy and yet found success - an important lesson for younger investors. You can watch the whole interview here).

Here is an interesting conversation with Ted Weschler, who along with Todd Combs manages the investment portfolio at Berkshire Hathway. The podcast talks about Ted's two lunches with Warren Buffett leading to the offer to work at Berkshire. It also traces Ted's earlier investment journey, and later talks about his reading habit. A well rounded conversation.

I quite enjoy reading investor profiles, and Frederik Gieschen of Neckar does a wonderful job of collating them. In a recent two part series (part 2 is paywalled), he profiled David Tepper.

The following best describes David:

"Investing with David is like flying, with hours of boredom followed by bouts of sheer terror," a long-time client commented. "He's the quintessential opportunist, investing in any asset class, but you have to have a cast-iron stomach."

After successfully buying distressed debt in 2002, Alan Fournier gave Tepper a pair of brass testicles, “cartoonishly huge and grotesquely veiny” as New York Magazine described them. The balls came with a plaque inscribed with the words ‘The Most Valuable Set of All Time.’

In the latest episode of The One Percent Show, Vishal Khandelwal interviews Kuntal Shah. Kuntal bhai unpacks so much wisdom in this single episode, leaning on his extensive reading and deliberations. He also shares a long list of book recommendations all through the episode. Great listen, and a wonderful start of the interview with the twelve equations:

Enjoyed having a conversation with @safalniveshak on wide-ranging topics !! Everyone's question papers in life are different so the answers ought to be different too. So go by your inner scorecard but do incorporate valid and logical outside views from eminent thinkers.

Enjoyed having a conversation with @safalniveshak on wide-ranging topics !! Everyone's question papers in life are different so the answers ought to be different too. So go by your inner scorecard but do incorporate valid and logical outside views from eminent thinkers. My conversation with @Kuntalhshah on #TheOnePercentShow. Kuntalbhai talks about - - 12 equations of life and investing - dealing well with uncertainties - lessons from financial history - business value drivers - and much more. Enjoy the conversation! https://t.co/YmCCWZm1Hj

My conversation with @Kuntalhshah on #TheOnePercentShow. Kuntalbhai talks about - - 12 equations of life and investing - dealing well with uncertainties - lessons from financial history - business value drivers - and much more. Enjoy the conversation! https://t.co/YmCCWZm1Hj Vishal Khandelwal @safalniveshak

Vishal Khandelwal @safalniveshakWith the following description, could you guess what business is this:

"Researchers were allowed to spend 15% of their time investigating whatever they chose. Further, ...employees could push a suggestion past their direct report in the event they were getting pushed back on an idea....Once a researcher had proved him or herself to be an innovator (through new patents and products), their name was published in the * Innovators Hall of Fame, next to their patent, and was then allowed to spend up to half their time on projects they choose."

If you thought the above described Google or 3M, you were wrong. It is, in fact, the description of a textile company that this article talks about to highlight the importance of people in business.

"Interestingly, Milliken bet in completely the opposite direction to Buffett. As Buffett exited the textile business Milliken set about investing heavily in research and development to become the only remaining textile business in the US."

While addressing student, Mohnish Pabrai talks about why focusing on multibaggers is one of the best ways to invest. He also talks about how he found his 10-100-1000 baggers and some that he missed, why investors need not fear over-valuations - so long as stocks are not egregiously overvalued - and why you don't need many multibaggers. In about 40 minutes Mohnish lays down one of the simplest investment approach that most of us can follow along. Pair this with Peter Lynch's advice in the 'readworthy passage' section below to look for your own multibaggers.

Michael Maubossin always has interesting perspectives to shares. In a recent interview with Frederik Geischen, Michael talks about how he found and held on to Amazon during the dot com bust, his writings on feedback in investing, elite teams, expectations investing, and the likes. The bonus section was the most interesting where he talks about the contrasts in the position sizing philosophy of Soros and Druckenmiller with the fund management industry, the skills that portfolio managers should focus on, what analysts should focus on, among other things.

Howard Marks is a great thinker and a gifted writer. His memos make for very educating and very interesting reads. In his latest he talks about:

being unconventional in order to achieve differentiated outcomes, including being a contrarian;

taking the risk of being wrong (MS Dhoni, the erstwhile captain of the Indian Cricket Team would often be heard teasing his spin bowlers, saying "thoda aage daal; ek chakaa kha ke dikha". What he implied was that unless you risk being hit for a boundary, you wont get wickets easily. Howard Marks makes a similar point about investing);

a case study of someone who did the above, and one way we can all do the above.

While a lot of the memo is reproduction from old memos, it makes for a good read nonetheless.

"In short, being right may be a necessary condition for investment success, but it won't be sufficient. You have to be more right than others . . . which by definition means your thinking has to be different."

In a recent talk at Flame University, E A Sundaram asks some interesting questions:

Is it important to be the best?

Is the portfolio just a collection of best ideas?

How to handle periods of underperformance?

How long to wait with a stock that underperforms?

and a few more.

He also goes on to talk about his own investing process and his view on fees and skin in the game.

"You have to be good. You don't have to be the best"

I thoroughly enjoyed this interview of Roelof Botha on the Tim Ferris Show. Roelof is a partner at Sequoia Capital, where he joined in 2003. Formerly he was the CFO at PayPal. This wide ranging conversation provides a peek in to Roelof's early life as well as his motivations. It also covers some interesting concepts and lessons like: Investing with the Best, Ulysses Pacts, The Magic of Founder-Problem Fit, How to Use Pre-Mortems and Pre-Parades, Learning from Crucible Moments, and Daring to Dream. You can read the transcript here.

This is a long and interesting conversation between William Green (Author: Richer, Wiser, Happier) and Matthew McLennan, who oversees about $90 billion at First Eagle Investments. He’s co-head of the firm’s Global Value Team and also manages a few strategies. He previously spent 14 years at Goldman Sachs before being chosen by investment legend Jean-Marie Eveillard as his successor at First Eagle. Jean-Marie & Matt are the focus of a chapter in William’s book, “Richer, Wiser, Happier,” that explores how to achieve what Matt calls “resilient wealth creation.”

This is a short profile of a lessor known investor who not only shared his investment philosophy with Warren Buffett, but also a few investments. The article is also a reiteration of the buy and hold philosophy.

This is a fantastic conversation covering the journey of an institutional investor - from being an analyst to becoming a portfolio manager. Lots of wisdom shared around why people fail and what better practices can be adopted to not just avoid failure but to stand out. You'll find a lot worth highlighting in this conversation.

Here are some lesser known facts about, and lessons, from Sandy Gottesman who was a partner of Warren Buffett and Charlie Munger and a director of Berkshire Hathaway for nearly two decades. It's interesting to note Sandy's involvement in the trio's first investment as partners, as well as his influence on WB buying Apple recently. It's very unfortunate that Sandy didn't make a lot of public appearances.

I thoroughly enjoyed listening to this conversation of Russell Napier & Jeremy Hosking with podcast host Stephen Clapham. Russell is a global macro consultant and was earlier the Asia strategist at CLSA. Jeremy is a partner of Hosking Partners and was previously a founding partner of Marathon Asset Management in London. He is a co-author of the cult book Capital Account and its sequel Capital Returns. The conversation primarily revolves around the capital cycle and it's application in investing. Although, in order to explain the concept, the conversation does digress in to current macro and market conditions, but the views are interesting and different.

Soumil Zaveri of DMZ partners always has something interesting to say in his investor letters. In his latest, he presents a three variable framework for solving the investing equation. He posits that investors work backwards from an end-objective towards the right inputs needed to achieve it, and build resilience to stay the course in the crack of adversity.

Durgesh Shah (or Durgesh bhai as he is fondly called) is the founder director of Corporate Database and member of the governing body at Flame University. He is part of the famed Enam group, and a proprietary investor. The following is a dated multi-part interview series with Ramesh Damani (another famed investor in India).

Joel Tillinghast, who has something like $70 billion of assets under management, currently owns about 880 stocks. Joel became the manager of Fidelity's low price stock fund back in 1989, and he still manages it to this day. Over 33 years, he's racked up a spectacular record, beating his benchmark index by about 3.7 percentage points a year (despite being as diversified as he is). Peter Lynch, who hired him at Fidelity in the 1980s, has described Joel as one of the greatest, most successful stock pickers of all time. This podcast has Joel reflecting on his career, process, performance, and mortality.

Business Characteristics

Michael Porter recommended three business strategies for success: be better than competition, be cheaper than competition, or be different (operate in a niche). Which amongst these three do you think would be consistently better than the other two? This article tells you which one and why. It also suggests that investors adopt one of these strategies for successful wealth creation.

Warren Buffett rates pricing power as the single most important indicator of a business's strength. But what exactly is pricing power? Raising prices to pass on inflationary pressures is definitely not pricing power, claims this article, and then goes on to explain the kind of pricing power that investors should look for.

This article explains Morningstar's wide-moat investing framework. It makes the distinction between the three types of moats (wide, narrow, and no moats) and then goes on to explain five sources of moats. It also lists which of the five moats have worked best/least in the last 5/10 years. A good screener.

This twitter thread explains 'one of the greatest qualities a business can have: A LONG RE-INVESTMENT RUNWAY'. This is a very important concept that all long term investors must understand, and one that will help you identify and ride multibaggers.

This thread reminded me about this dated article that explained it best to me: Importance of ROIC: “Reinvestment” vs “Legacy” Moats

I had tried to condense my understanding of this concept here.

Two contrasting mental models about longevity and survival - The Lindy Effect, and The Turkey Problem. This thread uses the two models to help us think about the long term survivability of a business and why that matters to us as investors.

This is a slightly verbose albeit interesting analysis of multibaggers - stocks that go 10x or higher. It compares the various characteristics of mutibagger stocks at the beginning of their 10x or higher journey with the overall universe of stocks. It also breaks down the returns in to factors like earnings growth and multiple expansion. A helpful read on your quest to making 10x or more on your capital.

There is a lot of literature on how to make any company great. However, most of it focus on the 'what to do' rather than 'how to do'. Moreover, there is no way to account for the role of luck in a company's success. In order to overcome these shortcomings, the authors of this article shifted focus from what the companies did to how they thought. The result of this study was a set of three rules that made a company truly great. Next time you see a company thinking on theses lines, you'll know you've found a potential great one.

Here is some interesting research: two researchers tested a simple investment strategy that invested in the 100 most valuable brands after they were announced each year. They compared the performance of this portfolio of 100 brands with a portfolio of US companies matched by characteristics like valuation, size, profitability, etc., and another portfolio of companies matched by industry. The results might surprise you (not so much the outcome but the reason behind the outcome).

Market Lessons/Cycles

This thread draws lessons from the winners and losers of 2021 and in turn provides some good frameworks to think about stocks.

This two-part series draws 10 broad investment lessons from the market. When you look at the markets on a daily basis, it becomes difficult to see long term trends. Articles like these are good reminders of what matters or works in the long term. Some of my favourite lessons were 1, 4, 7, and 9. You can pick your favorites here: Part 1, Part 2.

How do market cycles occur? What causes the pendulum to swing from euphoria to crisis and back? That is what this article attempts to explains, using Hyman Minsky's ‘financial instability hypothesis’. It then goes on to explain how the venture capital world today may be having its own Minsky moment. A very articulate and interesting read.

Some quick lessons from the greats:

In a state of euphoria, many investors let their guard down. When stock prices are rising, and fast, focus shifts from downside protection to upside participation - invest first, investigate later. This is when investors are the most gullible - either of their own doing, or lured by someone looking to take advantage. The following are some such incidences:

First up is a story from 1890's about how one investor satiated the need of the general public to be guided into quick returns.

Next up is this incident from the 1920's about how margin investing didn't spare the father of value investing as well.

There is a similar story about margin that his protege Warren Buffett once shared about one of his partners.

This is an interesting fictional story of Wally who is the worst market timer of all time. Wally always buys at the top and exits at the bottom, until he inherits some fortune. The fortune comes with a restriction that Wally cannot sell his investments, and some other conditions. The outcome that Wally witnesses on his 91st birthday of his worst timing, but not selling is interesting. It tells you a lot about investing and stock markets. If you know someone who is always late to the stock market party, make her read this article.

A young investor regularly pens his investment lessons based on both positive and negative experiences. This is neat summary of 30 such lessons learnt over the course of a few years. I found myself nodding to most what the author had to say.

Here is some very interesting research on Growth Rates. The authors study the persistence of short term and long term growth rates, to conclude that predicting short term growth rates is easy while long term growth predictions are nothing short of chance. However, since we all need to predict growth, they provide some ways in which you can forecast short term and long term growth rates.

In a recent issue, we studied how growth rates do not persist over time. Following up on that research, this note looks at valuations in the context of growth rates not persisting over time.

Over the last few issues, we read some interesting research around the persistence of growth (#140) and multiples (#142). This is the third and final instalment of the series. It looks at the persistence of margins, and like the previous two, makes some very interesting observations.

Here is an interesting extract from Morgan Housel's Psychology of Money that demonstrates the important distinction between ‘getting wealthy’ and ‘staying there’. Investing is a journey and not a destination. Surviving matters the most.

This article is an ongoing list of some very well articulated investing thoughts. Lots worth highlighting here.

Valuations, Margin of Safety

Quality investors love to quote Charlie Munger on how the return on a stock will mimic the return that the underlying business generates on its own capital. They use this to justify Buy At Any Price investing. Debunking this myth, Jigar Mistry (a very gifted writer) claims that A good business and a good investment are two different things.

Here is another investor letter. This one, from Broyhill Asset Management, while discussing the current market outlook provides some interesting perspectives on the historical relation between starting valuations and prospective returns. The letter also provides a checklist observed by Goldman Sachs that characterizes an investment bubble (should be put up on your desk).

…is every stock now—maybe the market itself—more like an untethered balloon? When you stick a pin in a balloon, it doesn’t plummet toward the ground. It fires off at odd angles, sometimes shooting up to extreme heights, spinning and spiraling and seesawing—until it eventually runs out of air. Then it might drift back to the ground; or it might defy ration and reason, get caught in a stiff breeze—and rise up, and up, forever.

There is a general belief that as stocks get expensive, a correction is due. Investors often look at valuations to take exposure to, or exit from, stocks completely. However, this is not a good strategy, as this article explains.

Margin of Safety has traditionally been understood as the gap between price and intrinsic value estimate. However, given the inaccuracies that can creep into the an intrinsic value estimate, this article looks at margin of safety from a very different and interesting perspective. It also provides an interesting argument towards investing in slow growth businesses. This one is guaranteed to give you some fresh perspectives.

This article presents an interesting perspective to look at investments with. It breaks down price into multiple components that help bring clarity in why we hold the security and how/when do we expect to realise a profit from it. This is a different way of looking at your holdings and can help in categorising them in to different buckets so as to ensure reasonable diversification across different parameters of value.

Here is a very good explanation on why two companies with same earnings and same growth can have very different mutliples. This is a very important fundamental in investing that usually doesn't get talked about.

Portfolio Construction

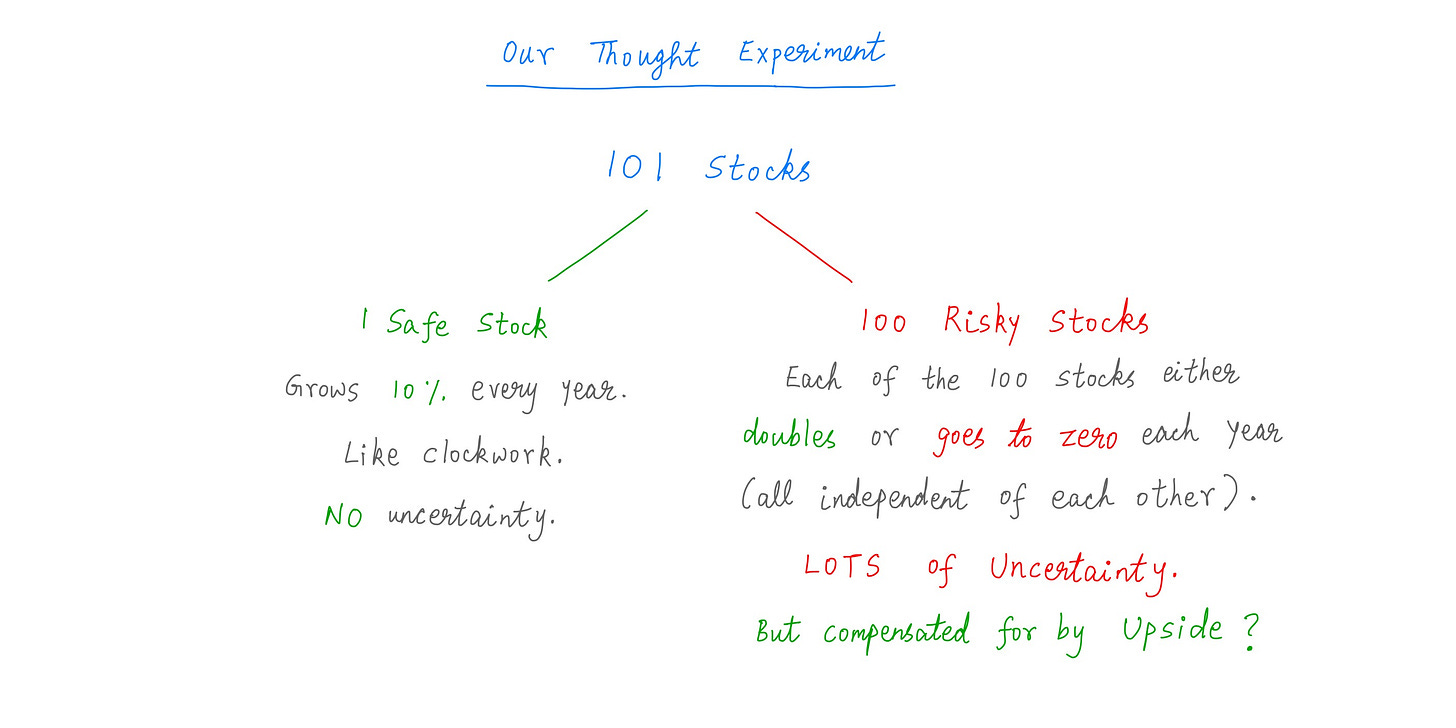

If you had two investment choices - one that mostly goes up, and other that mostly goes down - how would you build your portfolio? Most of us would want to invest only in the one that goes up. However, as this thread explains, the ideal investment would be a combination of the two. This is one of the best explanations of diversification that I have read in a while.

If you heard last week’s podcast of Joel Greenblatt, you would have heard him saying that he sizes his position not based on the upside potential but on the downside risk. This article elaborates on that using one of Bill Miller’s biggest losing trades.

Here is a very good thread covering two important portfolio management principles: minimizing correlation and rebalancing intelligently.

Investment Philosophy/Strategy

Investment Philosophy is a fancy term in the world of finance. Everybody has one. However, not everyone uses it effectively. Most times, it serves as a good marketing tool. Some, however, know its real power, like the author of this article who breaks down the philosophy in to a few basic questions.

This is a slightly touchy subject, especially with hardcore fundamental investors. Technical Analysis, or the study of price movement, is in complete contrast to fundamental analysis, as one starts with price while the ends there. More importantly, one is backward looking, while the other is forward looking. This post suggests that marrying the two contrasting ideas - like most things in investing (strong convictions loosely held) - can help investors in making some decisions better.

The benefits of investing in good quality businesses are widely known. However, quality investing has two shortcomings and an important tradeoff that investors today need to think of. This article explains.

Investing in high quality - wide moat - businesses has become a very popular strategy. This is especially true in a country like India where an entire decade of low growth and low inflation pushed everyone towards high quality consumer businesses (as that was the only segment that grew at a reasonable rate). Today, investing in quality businesses is being touted as the only investment strategy by some. While it is indeed a good investment strategy, it remains misunderstood. As this article explains: high quality businesses can generate high returns under the right conditions, but their best feature is safety.

Here are five simple but powerful questions that every investor should answer before making an investment. Since investing is as much about the state of our mind, as it is about its ability, these questions will ensure that you are in the right state before making a decision.

Two pieces of advice(from the same author) that are worth their weight in gold:

How to Succeed as a Sell Side Trader (dont go by the title; the advice applies as much to a long term investor as much as it applies to a trader. Strongly recommend reading this)

Everyone should read this thread and internalise the lessons.

Using the above thought experiment, the author teaches us that:

we should approach investing as a 'satisfying' game. Not a 'maximizing' game;

it's hard to distinguish LUCK from SKILL;

we should aim for consistency over supremacy.

This post explains why Conviction is one of the most important skills, and provides a framework that will help you build conviction. If you are an investor in direct stocks, you'd do well to read this well articulated post.

This short article makes two very interesting observations: a) having a thematic flavor helps a fund outperform; b) fund managers with specific expertise in their educational backgrounds do well managing thematic funds in their area of expertise. Read on to know why.

Risk / Regret Minimisation

The investment field is full of regret landmines. There is regret of not investing in to something, and there is regret of investing in to something. There is regret of buying something too soon, and there is regret of buying something not too soon. There is regret of selling too soon, and there is regret of holding on too long. You get the gist. These regrets are inescapable. But we can chose not to suffer at their altar. This article tells you how. Put it up someplace that you can see regularly.

Stock markets can be rewarding in the long run. However, in the short run, they can be stressful, irrational, as well as intimidating. Short term setbacks are often the price of long term rewards. However, these set-backs are seldom easy to endure. This short thread provides a 'Tough Times Playbook'. (the 2-page exercise in the thread is worth practicing)

A 10% correction in the market could mean differently to different people. Someone with a long investment horizon might rejoice a 10% correction as an opportunity to buy the dip. On the other hand, the same 10% correction may delay someone's retirement by a year or two. Risk, therefore is perceived differently by different people. Or, as this article puts, risk is deeply personal and always contextual.

Are past mistakes good teachers for future actions, or do they act as an anchor holding us back, or both? That is the question that this post is attempting to answer. It contemplates whether we are better off forgetting our past or not.

One of the ways in which we can reduce our investment regrets is by basing our decisions not on narratives or the past, but on probabilities. A good investment in one in which the odds are in our favor, although calculating odds doesn’t come intuitively to us. This article helps.

Mistakes are one of the best teachers. And yet, we seldom learn from them. This thread explains how we can perform post-mortem on our investment decisions. Done right, his exercise can help boost performance meaningfully, claim the authors.

Mental Models & Behavioral Biases

Decision Making

All the analytical rigour and the emotional stability in investing is towards one end: making good decisions. Every time you look at your portfolio, you make a decision to buy/sell/hold. Doing nothing is also a decision in itself. Given how integral decision making is to investing, it is imperative that we develop some models and checklists to make it more effective:

Here are five models to think about when making decisions, from Annie Duke's book Thinking In Bets

If the above five models don't help enough, then this article provides a nifty process that you can use to make tough decisions.

One of my professors used to assert that 'you've understood a concept well only if you can express it as an equation'. This article, breaking down decision making in to its key components, will tell you why he was right. This is one of the best articles on decision making that I have read so far.

We usually look at behavioural biases from an individual perspective - 'things I need to watch for'. But these biases are also exhibited by large groups, like the market as a whole. By building a system to identify such group behaviour, we can improve our own investment decision making, claims this article. It presents an evidence/expectation based quadrant as a model to read the market mood and then provides some strategies for dealing with each quadrant.

We make numerous decisions every day - in investing, and in life in general. For an activity that has such a high leverage on our life outcomes, we don't put enough effort in trying to make the right decisions, according to this article. We tend to favor the inside view over the outside view, it claims. It then goes on define the difference between the two, and tells us how we can better incorporate the outside view.

Bayes theorem is an important concept in probability and has wide applications, including in AI and ML. Simply put, the theorem states that we should update the prior probability as and when new data surfaces. Mathematically, however, the it can be a little tedious to understand. Here is, to my mind, the simplest and most effective explanation of Bayes Theorem.

We have often said here that investing is a fine art of balancing two opposing forces - like, strong convictions, loosely held. On similar lines, every investing decision has to sides - risk and returns. And not matter what you decide to do, something will always hurt. Let this brief article explain.

"Everyone must choose one of two pains: The pain of discipline or the pain of regret.”

- Jim Rohn

The Disposition Effect - selling winners early and holding on to losers - is something that most of us are guilty of. Research, however, shows that one type of investors are more prone to this error than others. This article explains why, and also suggests how we can try to reduce this error.

We usually see a lot of models that help us make a decision or avoid it altogether. Not a lot is usually said about situations where the make or break point is evaluated after the decision is made - i.e. should you continue or quit a project after having started it. This article does exactly that. It provides two decision models that help to cut your losses early - an activity that can improve your returns.

Behaviour Biases

Here is a light read on the follies that draw investors towards assets with lower expected returns. Pertinent to read this in a bull market.

“Much of our investment activity involves doing things that make us feel good in the moment. We can then repent at leisure.”

It is easy to think that we can buy the dip, whereas in reality it may be very difficult to live through the dip. This difference between imagining a situation and actually experiencing it is, in some ways, a behaviour gap. Morgan Housel explains it here.

We often weigh the same information differently. For instance, if a lesser known investor gave you a stock idea, chances are you'll not pay much attention. However, if a well known investor explained the same idea to you, you'd want to act on it. The idea is the same, however, where it comes from matters. This is because we believe that the well known investor's process is superior to the lesser known investor, simply from the fact that the former is more successful and hence well-known. This belief in the strength of a process based on the outcome is a behavioural bias called Resulting. This short article explains it very well using the example of Netflix.

This fantastic long-form article talks about an interesting mental model called The Hummingbird Effect, and it's opposite called The Poison Tree Effect. If you want to understand how the invention of the printing press led to the development of micro-biology, or how some of the great economic collapses came to be (and how some then led to rise of tyrants like Hitler) then you must definitely read this article. The authors ability to connect ideas across domains and time horizons is truly commendable.

On similar lines, a model that will help appreciate the movie Red Joan (available on Amazon Prime) which is loosely based on history is Mutually Assured Destruction. The movie is about a lady who leaks British nuclear secrets to Russia, helping them develop their own nuclear bomb. While she was initially branded as a traitor, she defended herself as a hero, and indeed she was. This article will help you understand why.

This article looks at two fallacies w.r.t. investing: price anchoring and narrative fallacy. While each has its own pitfalls individually, the two together can have a serious impact on your investments. Some good examples in the article as well.

In his classic style, Morgan Housel explains why we experience 'once in a lifetime' events more than once. A good lesson in probabilities.

'‘With a large enough sample, any outrageous thing is apt to happen”

Below are two articles that make for a very interesting read. Both talk about the wisdom of the crowd - how it is a powerful model of prediction, and how the model can break easily (i.e. why it doesnt work in the markets often):

According to Rene Girard, the originator of the Mimetic Theory, 'Man is the creature who does not know what to desire, and he turns to others in order to make up his mind. We desire what others desire because we imitate their desires.' While there are many implications of this theory, one of the them is related to Success. Since most of us don't know what we want, we cannot define success by our own measures. We then look to the crowd to tell us if we have succeeded or not. This outward looking creates an undue pressure on us. Morgan Housel narrates two stories from the same event in history to highlight such pressure, and to contrast external vs internal impulses. Whats your north star?

In his latest, Morgan Housel asserts, "If you find something that is true in more than one field, you’ve probably uncovered something particularly important. The more fields it shows up in, the more likely it is to be a fundamental and recurring driver of how the world works." He then goes on to list a number of such observations that apply across fields, in life in general. A mini-course in a number of mental models.

Our lives, and most things we experience, are more random than we think they are. Drawing from the book 'The Drunkard’s Walk' by Leonard Mlodinow, this article explains a number of fallacies that we exhibit in ignoring randomness.

“It is easy to believe that ideas that worked were good ideas,… and that ideas and plans that did not were ill conceived… But ability does not guarantee achievement, nor is achievement proportional to ability… A lot of what happens to us… is as much the result of random factors as the result of skill, preparedness, and hard work… We ought to identify and appreciate the good luck that we have… [and] appreciate the absence of bad luck, the absence of events that might have brought us down, and the absence of the disease, war, famine, and accident that have not—or have not yet—befallen us.”

- Leonard Mlodinow

The following are two interesting write-ups from Morgan Housel:

Incentives - The Most Powerful Force In The World: We all know that incentives drive behaviour. Yet, we under-estimate their influence. In this post, Morgan presents some unusual perspectives on how incentives can drive bad behaviour in even the sane people. Some interesting real life examples here.

Engaging With History: We all know that history rhymes, even as it doesn't repeat. And yet, there is not a lot that we learn from it. In this post, Morgan Housel strongly advocates that lessons from the past deserve more attention that they get.

The modern society frowns upon rituals and considers them a result of superstition. Yet, we see them exist in everyday life; for instance in the world of sports. Looking into the rituals followed by Tennis star Rafael Nadal, this article explains why rituals are more than superstitions. Quite revealing, this article.

Personal Development

Time Management / Productivity

There is no much written and consumed about productivity that it is now dubbed as 'productivity porn'. IMHO productivity is mis-understood as trying to do more in less time. To me, productivity is more about doing things efficiently and effectively. The following will help you do this:

Our minds are like monkeys, jumping around all day. We all experience those times when we just cannot focus on the task at hand. Here is a simple system that teaches you to match your state of mind with an appropriate task to enhance productivity (unlike most productivity porn about to-do lists and apps, this one is a rather simple system that involves only you and your mind). Good short read.

Most of us consume a lot of literature on personal development and productivity. While there is no harm in wanting to improve oneself, the problem with this approach is that you end with a lot of advice and trying to do too many things at the same time. The end result is that we usually fall back to where we started. That’s where this article helps.

Firstly, it suggests that instead of working on multiple habits, we should focus on one, and incrementally improve on it. Small changes can go long. Secondly, and more importantly, it lists three major habits and the ideal order that most of us should focus on. Mastering these three habits will make it easy to work on the others in the future.

This article is for everyone that manages a team, no matter how big or small. In about 10-11 sentences, the article will tell you why you are not being an effective worker, and why you are always busy. Short but hard hitting.

We've spoken earlier of how there is so much written about productivity and time management that it's dubbed as productivity porn. The problem with most productivity advice is that it is given in the form of a template - a one solution fits all format. However, given varied work cultures and responsibilities, this one-size-fits-all approach falls short. That is why this article suggests that how to manage your time depends on what responsibilities you bear at work. To be clear, the article advocates that we all manage our schedules, and to that extent it is part of the porn catalogue. It, however, provides more utility that your usual prod-porn.

Knowledge Management / Learning / Personal Growth

This five page extract from a speech delivered in 1993 is amongst that best meditations that you can read on personal growth, lifelong learning, motivation and the likes. This talk reminded me of two others that we have looked in the past:

@SeanDeLaney23 I equally like these two as well: Managing Oneself: hbr.org/2005/01/managi… Common Denominator of Success:

@SeanDeLaney23 I equally like these two as well: Managing Oneself: hbr.org/2005/01/managi… Common Denominator of Success:

When it comes to work, the general advice offered is on the lines of: dream big, do something that is at the cross-roads of what you like, and what you are good at; intern with those you admire; iterate until you succeed; study what works and what don't, etc. Here is a story of a creator that drank this cocktail advice and created a character that all of us have enjoyed. And in the process, joined the billionaire club while being mostly under the radar. What an inspiring story!

Talking about success, is there is secret to it? Most would say hard work topped with luck. This thread, however, suggests otherwise. The author claims that success is not about working harder, having better ideas, or knowing the right people, but about not obsessing over what to work on & start looking at how you work. It's not about the goals, but about the systems.

How to deal with information overload? Two short videos that provide some frameworks:

Frederik Gieschen distills some of the key lessons from Tiago Forte's book 'Building A Second Brain' in this post. The book talks about the need to organise information as well as the need to make smart (and progressive) notes for better retention. Tiago offers an interesting framework for this, which he calls the CODE framework. My own system, while not an exact replica, draws heavily from this framework.

The need to device a system to filter signal from noise cannot be over-emphasized in the age of the internet where we are bombarded with new information every second. This article lists 7 “Tricks” for Evaluating Information outlined by Nobel Laurette Richard Feynman in his book.

What gets measured gets managed. It's the same with progress - it is determined by how you measure it. Therefore, before you set out to achieve something, make sure you are setting the right targets: a hefty bank balance, or a life changing product, or number of lives improved. This article explains.

As we get to the end of the year, it is important to look back at how the past twelve months have transpired for you, and then plan what you want from the next twelve. Here is a template that will help you review what’s working, what isn’t, and how you can improve moving forward. (Watch the video accompanying the presentation here for a better understanding).

Feelings - Happiness, Misery, Stress etc

Misery is universal, while happiness is a niche. It's hard to define what makes us happy, but easy to figure what makes us sad. Using the power of inversion, this article lists some miseries to avoid in order to live a more happy life.

Why is it that a lot of successful people and business find it difficult to succeed further? Why is it that most achievers hit a glass ceiling? Greg McKeown, author of the book Essentialism: The Disciplined Pursuit of Less, claims that this happens as success is a poor teacher, and it leads to chaos. He explains further in this wide ranging talk by stitching together trade-offs, FOMO, JOMO, Gandhi, and Salt March (Dandi March). In case you are wondering that this is a problem for highly successful people and not for me, then maybe you want to consider the idea that the lack of success is probably due to an undisciplined pursuit of more. This talk is as much for those who don't think they are successful as much as it is for someone successful.

They say in investing that you should buy the dip. Dips, however, occur not just in markets but also in life. No matter what activity we undertake, we all experience a dip. This article explains these dips, how to survive them, and why surviving them is important.

[Also do read the follow-up article linked at the end of the article].

"Anything substantial that’s worth doing will have the dip. If it did not have a dip, everyone would be doing it easily and we wouldn’t call it a substantial achievement. A different way of saying it is that far too many people give up when they reach the dip and those who can cross the dip are the ones who taste success."

We often complain when things don't work out the way we like. We detest pain and suffering, not realising that this pain and suffering is what shapes us. As Victor Hugo said, 'Adversity makes men, and prosperity makes monsters'. Let this article explain: What is Chasing You?

The above article reminded me of this story shared by Morgan Housel:

"Gabby Gingras was born unable to feel pain. She has a full sense of touch. But a rare genetic condition left her completely unable to sense physical pain.

She can fall off her bike and get up like nothing happened.

Stub her toe and not even notice.

You might think this is a superpower, or an incredible gift. But her life – profiled several times in the last decade – is dreadful.

The inability to feel pain left Gabby unable to distinguish right from wrong in the physical world. It’s one of those things that’s easy to take for granted until you see what happens when it’s gone. One profile summarized a fraction of it:

As Gabby’s baby teeth came in, she mutilated the inside of her mouth. Gabby was unaware of the damage she was causing because she didn’t feel the pain that would tell her to stop. Her parents watch helplessly.

“She would chew her fingers bloody, she would chew on her tongue like it was bubble gum,” Steve Gingras, Gabby’s father, explained. “She ended up in the hospital for 10 days because her tongue was so swelled up she couldn’t drink.”

Pain also keeps babies from putting their fingers in their eyes. Without pain to stop her, Gabby scratched her eyes so badly doctors temporarily sewed them shut. Today she is legally blind because of self-inflicted childhood injuries.

Pain is miserable. Life without pain is a disaster."

The following are two long but very interesting reads:

The first one, rooted deep into philosophy, is a meditation on why we are never satisfied. Here is a summary courtesy Swanand Kelkar and Saurabh Singh (who originally shared the article):

The second one approaches the problem from the other side. Instead of asking why we are never satisfied, it seeks to find what makes us happy? This is probably the longest running research project where for 72 years (as at 2009), researchers at Harvard have been following 268 men who entered college in the late 1930s - through war, career, marriage and divorce, parenthood and grandparenthood, and old age - to find the answer to this question. The findings are quite interesting and unexpected.

Dr. Robert Sapolsky, while talking about his 1994 book Why Zebras Don't Get Ulcers, provides a seemingly logical explanation of what stress is and what it does to our body (including the kind of stress signals you send you body when you go for that 5k run). You may have heard or read about this topic, but you would not have come across anything close to how Dr. Sapolsky puts it. He is a talented scientist and a gifted speaker. This talk is a mix of humor and horror.

This personal account of a 'military spouse' encourages us to live each moment to the fullest. A very nice read (and no, its not about death). Some quotes from the article:

"Live like you're running out of time—because you are."

"Being human is to exist in a world of finite time, vulnerability, risk, and uncertainty. In this milieu, you have to make a choice—play it safe and live small or go all in."

"All we have is now. Take nothing for granted and make it count. Build a life that would make goodbye hurt and leaving hard."

"if the ending hurts, it usually means something went right."

One of things that doesn't come easily to most of us, no matter what, is the ability to accept failure (or fate). Here is one note and two small audios that I think might help build that ability a little:

Reflecting on existence of 44 years, the author of this article shares an interesting episode from Thomas Edison's life and provides us a good template to accept the vagaries of life and markets.

This short podcast lists a few failures and rejections that some well-known personalities have had to face in life, to encourage you to think that nothing great can happen without failure. -

Reiterating the above is this other episode that lists all the failures that preceded Abrahim Lincon becoming President and well-known.

Skill Enhancement

We've always thought of and looked at compounding from the perspective of investing and habits - small incremental changes over a long period of time can lead to outsized results. Interesting, this article presents the idea from a skills perspective. It agues that sometimes a combination of seemingly mediocre and disjoint skills can create great outcomes - just as when you mix two metals to create an alloy. The article then goes on to list some skills/behaviours that can work wonders when combined together.

Principles distilled from interviewing world-class performers by Sean DeLaney. This should be one of your top listens this weekend. (Thanks for doing this Sean, really enjoyed it 🙏🏼.)

I enjoyed the talk so much that I transcribed it for a slower consumption. You can access it here.

When it comes to developing skills, or excelling in an activity like sports, it easy to reach average levels. Its a little bit of work to get to above average levels. However, from there on, the gradient of improvement vs effort becomes very steep. There is very little improvement for increased efforts, thus making it extremely difficult to become the best at something. There is, however, an alternative path to the top that is less tedious and requires smart work over hard work. This article explains: How to Become the Best in the World at Something.

We all know that role that patience plays in investing, or in any long tenured activity. However, not all of us are born patient. Some of us like activity and cannot sit idle. How then do we play long tenured games? This post provides a possible solution what the author calls Functional Patience. While we may not be patient generally, we can learn to develop patience for certain functions.

Ideation / Meditation / Stoicism

Doesn't it often happen that you are thinking about a problem and cant seem to find a solution. Then, at a seemingly random moment, Eureka strikes!! Archimedes found it in the bathtub, many find it on long walks, some find it in their sleep. There are many way that Serendipity strikes us. But is that a way to make this deliberate rather than random? This article provides one way to do, somewhat on the lines of what Charlie Munger prescribes.

We are all aware of how the subconscious solves some of the tougher problems - the shower thoughts, or the famous Eureka moment. Given this knowledge, it is imperative that we create empty spaces for the subconscious mind to work, and ensure that it works on the right problems. While a lot has been written on the former (long walks, writing etc), not much has been written on the latter. This article tells you how and why the top idea in your mind matters.

This article lays down 15 rules that stoics follow in general. While the number 15 may sound large, I see them fitting in to three large buckets: how we deal with ourselves, how we deal with others, and how we deal with external circumstances. Reading this article is equivalent to reading a book on the topic.

Two interesting short videos well worth the time:

A story from the Brahmavar Upanishad about Lord Indra that applies to all our lives

A snippet from the movie The Founder about the wonders of Persistence (h/t to Sean Delaney for sharing this)

Ray Kroc: "Now, I know what you're thinkin'. How the hell does a 52 year old, over-the-hill milkshake machine salesman... build a fast food empire with 16,000 restaurants, in 50 states, in 5 foreign countries... with an annual revenue of in the neighborhood of $700,000,000.00... One word... PERSISTENCE. Nothing in this world can take the place of good old persistence. Talent won't. Nothing's more common than unsuccessful men with talent. Genius won't. Unrecognized genius is practically a cliche. Education won't. Why the world is full of educated fools. Persistence and determination alone are all powerful."

Good ideas are rare. But can they be programmed? Can you find a way to improve the quality of your ideas? Well, the author of this TED talk seems to think so. Inventor Mark Rober talks about How to Come Up With Good Ideas.

Here is an interesting parable that could be applied to most things in life. Very intelligently worded, the article will leave you with great clarity in how you should navigate this world.

This article lists three rare skills that if you master, can bring you peace of mind.

Upon turning 28, David Perell (twitter sensation and writing coach) pens 28 short pieces of life advice. Some very interesting snippets of wisdom here.

This post makes an important distinction between rudimentary and evolved simplicity. It posits that simplicity sits on each side of complexity, with the order being rudimentary simplicity-> complexity -> evolved simplicity. A good example of this is investing, which is a complex occupation. Players like Warren Buffett are evolved, having mastered the game. We all read and listen to Buffett, but most don’t come close to his accomplishments. This is because we sit in the rudimentary camp. This post explains the three stages in more details, and also prescribes how we can traverse from rudimentary to the evolved state.

Physical Well-being

We seem to be the most focused on exercise today compared to history. And rightfully so - the importance of exercise cannot be overstated. However, maybe we have the concept of exercise wrong in our head, claims this article. It quotes the example of Japan - a country with low obesity rates and a leader in longevity - that has not much of a workout culture. Does this mean that exercising has no impact on life span or weight loss? Read on to find out.

When it comes to forming or breaking out of habits, it is usually willpower and discipline that get all the attention. However, as the below excerpt from Farnam Street's Newsletter explains, your environment plays an equally, or more, important role. Willpower is like a muscle, which can break down when overworked. Environment, on the other hand, is like a protein that can help rebuild and keep that muscle strong.

"Eventually, everyone loses the battle with willpower; it’s only a matter of time. Consider my parents. Neither of them smoked when they joined the armed forces, but it didn’t take long for them to join their smoking co-workers. At first, they resisted, but as the days turned into weeks, the grind of saying no when everyone else was saying yes wore them down. Decades later, quitting proved nearly impossible when they turned to willpower. Everyone around them smoked. The very same force that encouraged them to start was preventing them from stopping. They were only able to kick their habit when they changed their environment. They had to find new friends whose default behavior was their desired behavior.

What looks like discipline is often a carefully created environment to encourage certain behaviors. What looks like poor choices is often someone trying their best to use willpower to go against their environment.

The people with the best defaults are typically the ones with the best environment. Sometimes it’s carefully chosen, and sometimes it’s just plain luck. Either way, it’s easier to align yourself with the right behavior in the right environment.

The way to improve your defaults isn’t by willpower but by creating an artificial environment where your desired behavior becomes the default behavior.

Joining groups whose defaults are your desires is an effective way to create an artificial environment. If you want to read more, join a book club. If you want to run more, join a running club. If you want to exercise more, hire a trainer.

Your environment will do a lot of the heavy lifting for you if you align it with where you want to go."

* * *

That's it for this weekend folks.

Have a wonderful week ahead!!

- Tejas Gutka

You can read the past issues in the best of series here:

A true treasure trove. Thanks a ton Tejas! 🙏🏼

This post is a goldmine Tejas! And appreciate you sharing the Li Lu article 🙏