[The Weekend Bulletin] #57: Rebooting 2020 - Links Worth Revisiting

A collection of some of the best articles worth re-reading.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

Here's wishing you and your loved ones a very happy new year. Let's hope that 2021 brings along a bundle of joy, fulfilment, opportunities, and good luck.

We'll start the new year with a slight deviation from the usual issue.

This one is a collection of some of the best (in my opinion) articles that we've read through the course of the last one year, which makes it an unusually long issue (will probably be truncated by your email service provider). Further, replacing the regular sections are topics in to which most of these articles are divided, to make it easier to navigate.

More importantly, rather than being read over a weekend or a week, this one is meant to be consumed slowly, over time. The ideal way would be to just bookmark this issue and then return to it for a deep dive into a topic that you wish to learn more about.

Lastly, other than the division in to relevant topics, there is no order to the articles. Feel free to explore the way you deem fit.

Lessons From Some Accomplished Investors

Investing is a very interesting endeavour. There is not set formula to achieve success in investing - making it more art-like than science. Over the years, different people have adopted varied investment philosophies to achieve similar results. Below are the profile of/learnings from some such accomplished investors:

What better way to learn investing than by studying the Masters. And what better investor to study than the one who is the only investor to beat the S&P 500 for fifteen consecutive years. This article provides a good overview of legendary investor Bill Miller's investing philosophy and process.

He is the CEO of RARE enterprises, and a complete opposite of the investor who lends his name to that firm. Over his long career, he has worked was marquee investment houses like ENAM, ASK, RARE and the likes. He is credited with bringing to the big bull’s focus a private equity style of long term investing. He has many a multi-baggers under his belt. Yet, he lives a low profile life and his wisdom is rarely found on the web. Thus, you wouldn’t want to miss Utpal Sheth recounting his investing lessons from a career that has spanned nearly three decades.

The deepest insights sometimes reside in the simplest observations. In a rare (no pun intended!!) public presentation, Utpal Sheth (CEO of Rare Enterprises), delivers some deep insights for investors from simple observations. He observes that there are a few mega-trends that are underway at any point in time that transcend decades, geographies, and governments. Within these mega-trends, there are a few businesses that take a large share of value (market share, profits, or cash flows). Investors that can identify such mega-trends and the leaders within those trends tend to enjoy decadal out-performance.

This is someone who would probably be the world’s richest man in today’s dollars. Only the Rockefeller family would come close to the wealth that this man amassed through skilled trading for his family in the fifteenth century. Here’s a quick overview about this investor.

This investor is dyslexic, had an abusive father, would often run away from home, was sent to the navy, worked for nasa, and eventually started his own enterprise. His fortune, however, didn't come from some flash of entrepreneurial brilliance, but from a lifetime of buy-and-hold investing. Read here.

The most interesting was saved for the end. This is someone who probably holds the unofficial record of growing money faster and longer than anyone alive. Over three decades, he turned $11mn in $1bn - not for himself but for a college that boasts of the largest endowment per student in the whole of the US. The man's intelligence and humility is reflected in the fact that Warren Buffett considers him to be the only replacement for his father!!. Here is how the man did it all.

Veteran investor Durgesh Shah looks back at history for some important investment lessons. He talks about things to look at while making an investment as well as pitfalls to avoid. What better time to look at mistakes than the current downfall.

A classmate of John F. Kennedy at Harvard, intelligence officer during World War II, researcher at the Federal Reserve Bank, economics professor, money manager, pioneer in investment analysis, historian, expert on risk and author. No I am not referring to a group of investors, but a single investor whose thoughts are as interesting as his profile. A long and dated interview of Peter Bernstein by Jason Zweig.

“We’ve only owned 123 companies in 31 years and that includes the 21 we own today. The compounding is really what drive the returns. You align yourself with 20 or 25 great companies that can compound for not just years but decades oftentimes and they do the hard work for you." This is a great conversation between Dan Davidowitz & Jeff Mueller of Polen Capital and Tanos Santo of Columbia Business School on their investment philosophy and approach.

"Most managers try to buy high quality businesses with strong economic advantages or competitive advantage selling at a discount to intrinsic value. I think one of the reasons that active managers underperform consistently is because everybody's doing the same thing. They're all approaching from the same perspective. What we have found is more times than not, if you're just looking for high quality wide moat businesses selling cheaply today, you're going to find yourself in a lot of value traps." While it may sound surprising, WCM capital management does invest in to high quality businesses, but does it differently. In this talk, Paul Black talk's about the topsy-turvy journey of WCM Capital Management and their investment philosophy.

"In most walks of life, if you are correct you succeed. But in investing, it's not enough to be correct. If your correct answer is a consensus answer, then it's already in the price. Not only do you need to be correct, but also against consensus in order to make money." Rupal Bhansali, CIO & Portfolio Manager at Ariel Investments (named “Global Guru” by Forbes International Investment Report, “Global Contrarian” by Barron’s, “unconventional thinker” by PBS’s Consuelo Mack, member Barron’s Investment Roundtable which showcases “10 of Wall Street’s smartest investors”), talks about the difference between convential investing and non-consensus investing in this interview with veteran investor Ramesh Damani.

The following is such a wonderful story. The lessons transcend business, leadership, personal development, motivation, and then a few more. She is not really an investor in the traditional sense, but a great capital allocator (the president of Focus Brands at age 37, overseeing seven large brands of quick service restaurants!! ). She talks about her journey, success, and hardships in detail in the following interview:

While the above interview looked at her journey and personal traits, this one deals with her business lessons (specifically on brand, distribution, and leadership). While this interview has a number of business lessons, two of my favorites were Kat's perspective on brands being both relevant and different, and how price cuts can be used to increase revenues and margins. A very interesting conversation; highly recommended.

Chris Begg of East Coast Asset Management is a great thinker and writer. I used to really enjoy reading this investor letters, until they stopped coming after 2015. Therefore I latched onto this interview as soon as I found it. And like his letters, this one was so really worth the time spent (and worth re-reading once in a while). In this interview, Chris outlines his investment philosophy, provides a glimpse into his investment process, along with some checks that he has built to over behavioural biases, and about he tackles reading for himself and his team. He ends the interview with how reading philosophy has made him a better investor - not something you hear often. Lots of nuggets of wisdom in this one.

This is a crash course on understanding moat-based investing. While moats in investing may have been conceptualized by Warren Buffet, they were definitely popularized by Pat Dorsey. In this 22 page interview (treat this as a primer to his little book), he goes on to explain the different types of moats, how growth is not a moat, and how some moats can be mirage.

He is often referred to as the Guru of the Gurus. He also developed the Earnings Power Value metric to determine the value of the firm without using the DCF model in his book released around the 2002. In this talk, Bruce Greenwald updates his concepts around earnings power and franchise value, especially in light of the last ten years (increasing importance of intangible assets) that will also form part of the second edition of his book to be released next month. He provides a good framework for valuing business and identifying if growth is value accretive or not. Source:

Yen Liow of Aravt Global retraces his journey in to the world of investment in this aptly titled podcast, 'What Got You There’ and talks about (among other things) how he unconventionally used case studies to identify an investment philosophy that would help him deliver consistent and outsized returns over long periods of time. Of the interviews that I have heard and shared in the recent past, this one is probably amongst the very best. If I were an aspiring investor, I wouldn’t miss this one.

In a report titled ‘The Makings of a Multibagger’, Alta Fox Capital conducted a similar study (An Analysis of the Best Performing Stocks over the Past 5 Years) and was kind enough to share the findings (645 slides - but you can get a gist in the first 20-odd slides) with us. This is treasure-trove that needs not one, but repeated reading.

Here is something that all of us investors should be doing. Arisaig Partners looks at some of the its past investment decisions to identify the various biases that were are at play at the time of making those decisions. While the biases were not as apparent then, they surely are more recognisable with the benefit of hindsight. This is an exercise that if conducted regularly will help identify many of these biases pre-mortem rather than post-mortem. More importantly, then can also help identify a pattern of flaw in decision making over time. This note is praiseworthy in that not only did Arisaig Partners undertake this exercise, but they also made it public which is really commendable.

In this slightly dated interview, value investor Glenn Greenberg goes into the detail of his investment process that has helped him achieve the following: "We started with $40 million (in 1984), 2/3rds of which was family money. By 2006 we compounded that to 100x its original value before fees just by concentrated invest- ment in pretty pedestrian, easy to understand businesses that seemed under-valued. That meant no turnarounds, no crummy businesses, no highly competitive businesses, and no tech businesses, which we didn’t understand. It was boring stuff.”

Four short lessons from over a decade of investing by a self-taught investor. Not only are the lessons interesting, and relatable, but the author also goes on to talk about ten themes designed from his mistakes that he believes should be taught to CFA candidates. I believe that not just CFA aspirants, but many seasoned investors would also benefit if there ever was a classroom where these were taught.

He studied multibaggers, so much so that he wrote a book on them. Now he invests in companies that he thinks are potential multibaggers. And he has an advice for you: Look at the big picture, but don’t make too much of it. For, as he highlights from personal experience, these things don’t matter as much as other things do. Even if they matter, there are very few who can understand them well, consistently over time.

Growth and Moat Issues

Even high quality companies suffer growth pangs, making it imperative for investors to understand why this happens. This long form article looks in to some of the common factors that lead to a growth stall, arguing that most of the factors are internal to an organisation, knowable in advance, and are controllable by management. It also goes on to provide a checklist for managements and investors to identity such growth stalls in advance.

This article talks about the impermanence of economic dominance and moats. It makes a very interesting point: sometimes moats don't get eroded, but simply by-passed. New castles with better moats come up elsewhere.

Unpredictability of stock price movements in not the only reason that investing is difficult. It is also difficult because MOAT - regarded as one of the more important factors in fundamental investing - is not always reliable. For, as this article highlights, seemingly infallible moats can be filled, or an altogether new fort with different moat may come up elsewhere, leading to investors completely bypassing your fort.

Driving the point of legacy moats further, is Mark Walker of Tollymore Investment Partners in this interview on finding great stocks. He also reiterates Henrik’s findings that moats are often difficult to identify pre-mortem, and that past business performance need not sustain in the future. Some of his best investments, he says, are in businesses that were written off by investors as low moat businesses.

Risk

Risk is perhaps one of the most commonly used term in financial markets (second only to return). Despite its ubiquity and undoubted importance, it is often not clear whether it refers to volatility or the permanent loss of capital. Both sides of this argument are right, but wrong to believe that there is any single concept that can encapsulate investment risk, claim the authors of this article.

As much as we love to quantify risk, in reality, risk is uncertainty. It is a variable that is unknown and unknowable in advance. Since you can’t prepare for what you don’t know, that is where the real risk emanates from. This article narrates a very interesting true story to make this point.

Returns and Market Cycles

History can be a great teacher on one hand and misleading on the other. For instance, a deacde of strong returns may make you believe that future returns will be lower, since history has taught us that returns mean revert. However, history also teaches us that you would be wrong to anticipate such mean reversion soon. Read on to find out how mean reversion has happened in the past.

Valuations

"The Equity Yield Curve, a phrase of our choosing, is one tool – and one of the most powerful – for identifying and visualizing the enormous level of return often available from securities that have been ‘discarded’ or ignored by conventional investment practices. It is all about a rather insubstantial thing: time or, more accurately, time risk." This article talks about our inability to understand the convexity of the future - a concept similar to 'hyperbolic discounting' that we saw in Issue 12. In simpler words, why we underestimate the future earnings of companies.

What do PE multiples convey? Does a PE multiple of 10 imply cheapness over a PE multiple of 30? What conclusion should one draw by comparing historical average PE to current PE? More importantly, should two companies with the same earnings per share and similar growth rates be ascribed the same PE? While we widely use the PE multiple to value companies, our understanding of it is incomplete. This article serves as a primer on valuations and explains why different companies trade at different PEs.

Do starting valuations matter? Should you worry only about the quality of the business and its growth prospects, or should you also care about the price you are paying, even if your investment horizon is ten years? Are great businesses always great investments? This and more covered in this article (free article, but log-in required to access). If you are in a hurry, read from the section titled "Nifty FANGAM".

An underappreciated relationship in investing is that of ROIC and valuations. Investors focus excessively on growth of earnings while paying little attention to cash flows and RolCs. Another important relationship that is misunderstood is current expectations and future returns (or the impact of starting valuations. Borrowing from the book Valuations by Mckinsey (a great read) this article explains why the direction of ROICs and expectations embedded in current valuations matter for future returns.

Some Interesting Mental/Business Models

This is a crash course in mental models, or more appropriately, first principles. Peter Kauffman, author of the book 'Poor Charlie's Almanack', talks about the multidisciplinary approach to thinking - a very insightful yet simple talk. What makes this even more special is that there is not a lot of material that you'll find on Kauffman.

This mental model is a type of a Network Effect that explains hows things spread: from a disease in a population to a wildfire in a forest to a meme on social media. Called Simple Diffusion, it is the way things move somewhat chaotically across a network. While a little long and slightly technical, I would urge you to slowly consume this article and play around with the interactive charts. It will be well worth your time.

Luck

A new study looked at an old problem - while talent and efforts (inputs) follow normal distribution, why does wealth (output) follow power law (80:20 principle)? The answer is a catalyst that we all know, but do not acknowledge enough - Luck. It is the reason that the richest are not necessarily the most talented, and the most talented are not necessarily the richest.

Time Management / Focus

This is a human life, divided in weeks:

This is the life/achievements of some famous people (click to enlarge):

What about yours?

Hard hitting? Want to change your life? Read this article (also the source of the above images).

Our fast paced lives have often been compared to the hedonic treadmill: the faster we run to move forward, the more we stay in the same place (also referred to as The Red Queen Effect). In the quest for a better tomorrow we often forget to live for the today. We often look forward to have so much that we forget that the things that we have are the things that we looked forward to having in the past. A pause may be worthwhile, suggests this nicely illustrated article: Life is a picture, but you live in a pixel.

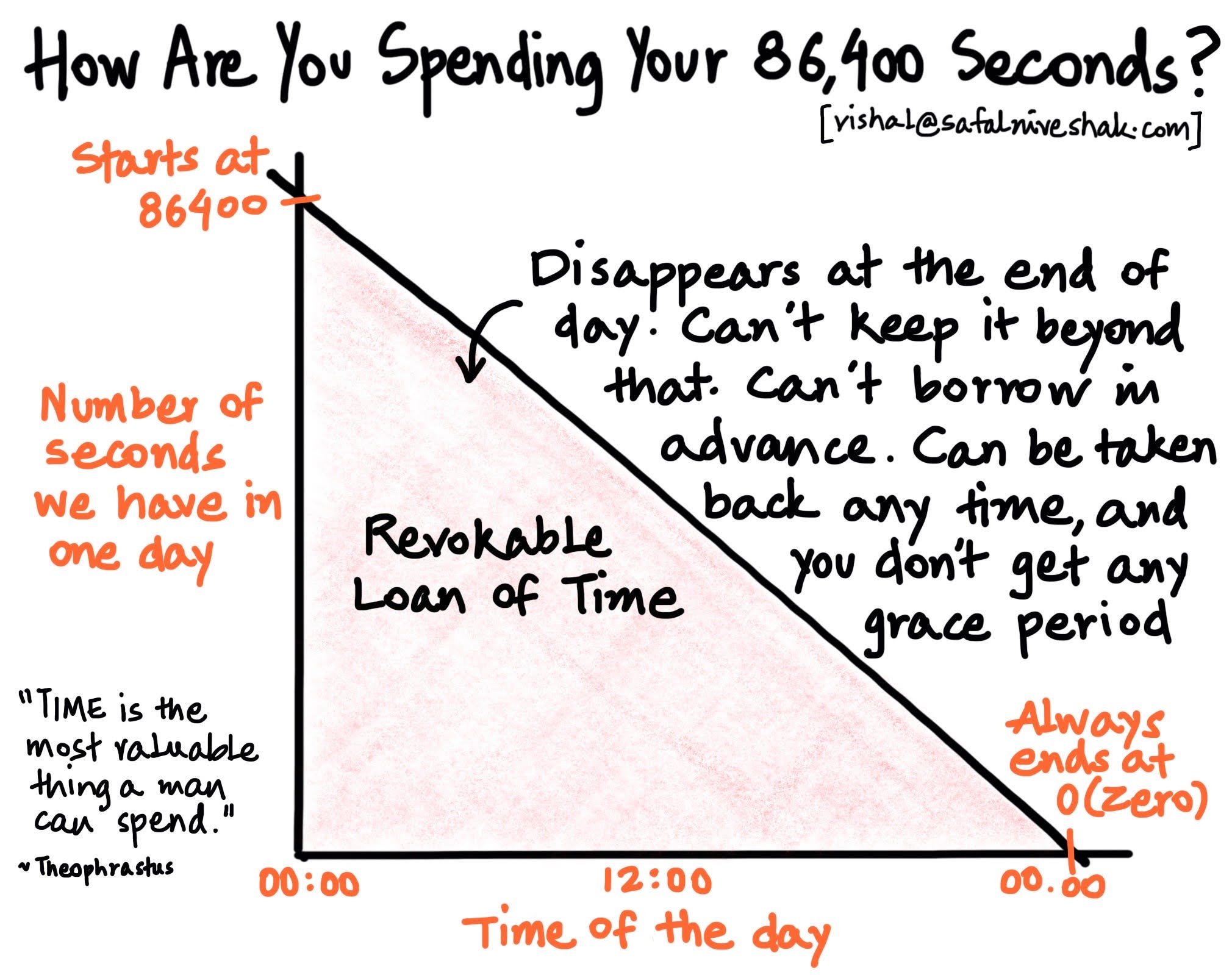

Let's say that you were given 100 bucks each day. You were free to spend those in any manner that you deemed fit, although you are told that you need to invest some of these 100 bucks to earn them back in the future. You have two implicit choices - either spend minimum on investing for the future, or save a lot for the future so as to get to a point that you wouldn't have to invest any. Most of us would, to a varying degree, choose the rest. After all, we chase financial independence. But why don't we think of of time as we think of money? Isn't our life bound by time, more than it is bound by money? What choice would you make if someone swapped the 100 bucks with 100 blocks of ten minutes each? Read more here. The rendition below is a nice representation of the concept:

There are two challenges that most of us face all the time, paraphrased below:

If time is the currency of achievement, why are some able to cash in their allocation for more chips than others? And in a world of rapid fire Slack messages, daily episodes of The Daily and Zoom calls up the wazoo - who on earth has the right to not feel rushed?

Productivity is fueled by raising attentional filters to keep unrelated or distracting thoughts out. But creativity is fueled by lowering attentional filters to let those thoughts in. How do you get the best of both worlds?

This well articulated article has the answers.

Personal Finance

This article would serves as a good starting point for the discussion on money vs wealth. Instead of differentiating between money and wealth, it talks about The Money Spectrum which serves as a good model for understanding how an individual moves through the different phases of having money: survival -> status -> freedom -> power.

This article is the most comprehensive meditation on building wealth that I have come across, outside of a book. It’s a great article to be read slowly, and repeatedly. If you are pressed for time, start from the section titled “8 principles to grow your wealth and income over time”, although I would urge you to persist through the entire article at least once.

Personal Traits

Here is a good lesson in humility. We are all gifted with some talent that makes us better than average. Over time, we take these gifts for granted, showing them off at every possible occasion. In a talk delivered in 2010, Jeff Bezos reminisces a lesson that his grandfather taught him: "It's hard to be kind than clever." Remember that you didn't choose your gifts, they chose you. However, you can chose your actions and let them define who you are.

One of Warren Buffet's many famous quotes is: 'Predicting rain doesn't count, building an arc does'. My own version of that quote is 'predicting rain doesn't count, carrying an umbrella does'. What they mean is that ideas are worthless without execution. And I thought that these quotes captured the idea so beautifully, until I read this article. While not as short as the quotes above, but in less than ten sentences it is the most impactful explanation ever. Here isa quote from James Clear that fits so well:

"The math of success...

Results = (Hard Work*Time)^Strategy

Working hard is important, but working on the right thing is more important. A great strategy can deliver exponential results.

Of course, the best strategy is worth nothing if you never get to work. Zero to the millionth power is still zero."

This mental model from Physics called 'Ground State' is the best personal development motivation that you'll need. Its a 2 min read, don't skip it.

We often confuse between intelligence and intellect. Intellect - ability to understand - is a gift, something that we are born with. Intelligence, on the other hand, is a like a muscle - something that can be improved with exercise.For example, between two people with the same intellect, one may be more intelligent simply because s/he spends more time thinking about problems. An easier way to understand this is in terms of sports - between two players with the same talent (hand-eye coordination), the person who practices more will have higher skills. Here is how you can improve your intelligence.

Approaching the above concept in a slightly different manner is Carol Dweck's fixed vs growth mindset. A fixed mindset looks at tasks as doable or impossible. On the other hand, a growth mindset seeks to operate just outside the boundaries of current abilities, thereby stretching the boundaries over time. This is a good place to start understanding this concept.

* * *

And that brings us to the end of this long issue.

Have a wonderful week and a great year ahead!!

- Tejas Gutka

[Jan 02, 2021]