[The Weekend Bulletin] #140: Predicting Growth, Deceiving Valuations, Functional Patience, Phil Fisher, Sandy Gottesman,...

...Serendipity in Berkshire, Disposition Effect, Decision Making, Seeking Awe, and more.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

Weeklong festivities begin in India starting this weekend. Our family is traveling with some friends this holiday season until next weekend. There will a break to this newsletter in this meantime. We'll resume from the first week of November.

Wishing you and your dear ones the best of this holiday season. Let the lights always shine bright.

Investing Wisdom

Here is some very interesting research on Growth Rates. The authors study the persistence of short term and long term growth rates, to conclude that predicting short term growth rates is easy while long term growth predictions are nothing short of chance. However, since we all need to predict growth, they provide some ways in which you can forecast short term and long term growth rates.

Some interesting materials on two investors:

A rare interview with Phil Fisher following the 1987 crash where in addition to the market conditions he talks about his investing philosophy, and contrasts his philosophy with Ben Graham's. The following is what I loved the most (emphasis added):

I have four core stocks that are exactly the thing I want. They represent the bulk of my holdings. I have five others in much smaller dollar amounts that are potential candidates to enter this group. But I’m not sure yet. If I were betting today, I’d bet on two and not on the other three. Each decade up to this one–there hasn’t been time to work it out for the Eighties–I have found a very small number of stocks, 14 in all, starting with 2 in the Thirties, that over a period of years made a profit for me of a minimum seven times the funds I put in and a maximum of many thousands of times my investment. Now I have gone into about three to four times as many additional securities in which I’ve made more money than I’ve lost. I’ve had losses, in two cases as high as 50%. There also have been a number where I have made or lost 10%. That’s almost the cost of being in business. But there are lots of cases where a stock has gone down moderately, and I’ve bought more, and it’s paid off for me enormously. These efforts were necessary to weed out the 14 where I have made the real gains. I’ve held those 14 from a minimum of 8 or 9 years to a maximum of 30 years. I don’t want to spend my time trying to earn a lot of little profits. I want very, very big profits that I’m ready to wait for.

Here are some lesser known facts about, and lessons, from Sandy Gottesman who was a partner of Warren Buffett and Charlie Munger and a director of Berkshire Hathaway for nearly two decades. It's interesting to note Sandy's involvement in the trio's first investment as partners, as well as his influence on WB buying Apple recently. It's very unfortunate that Sandy didn't make a lot of public appearances.

We often talk about the role of luck in investing and its influence on long term outcomes. Here is a very good story about the role of serendipity in creating Berkshire Hathaway in to the giant that it is today.

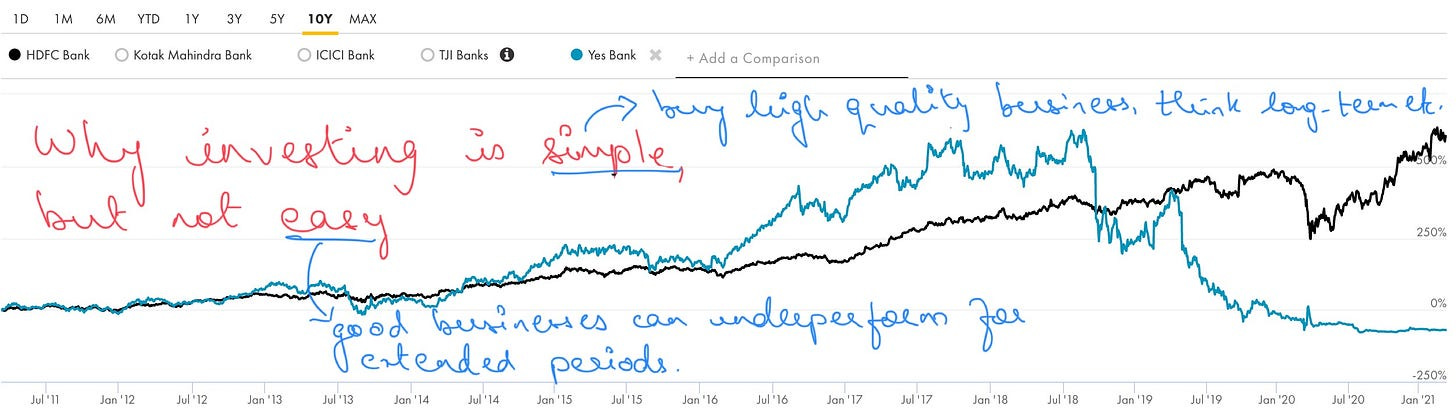

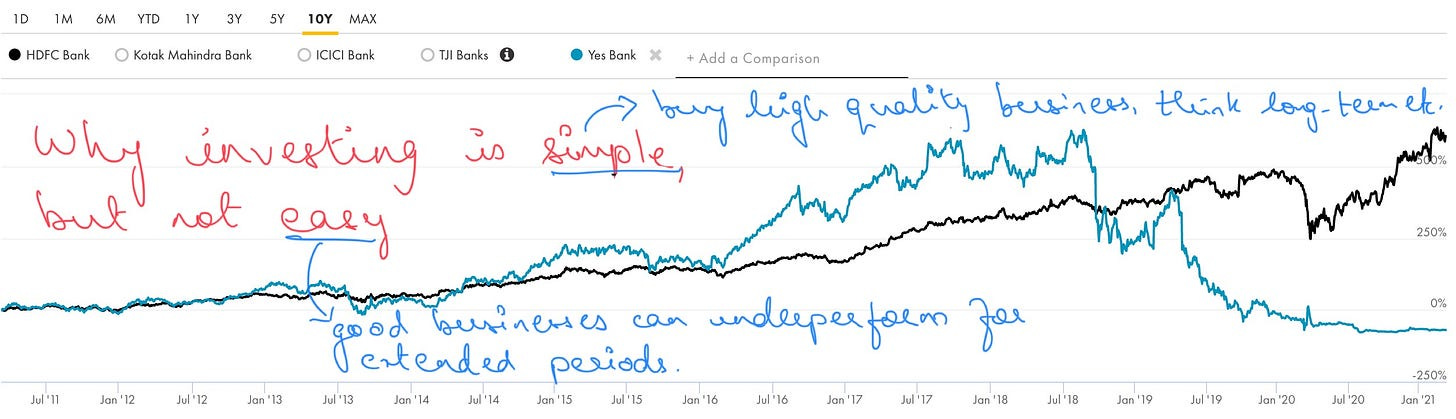

This bulletin has often reiterated that investing is simple but not easy. Echoing this sentiment is this thread that talks about how difficult it is to decipher what quality focused investors mean when they say 'paying up for quality'. A combination of quality and valuations are alone not enough for compounding capital - its not that easy.

Mental Models & Behavioral Biases

The Disposition Effect - selling winners early and holding on to losers - is something that most of us are guilty of. Research, however, shows that one type of investors are more prone to this error than others. This article explains why, and also suggests how we can try to reduce this error.

Investing or otherwise, one of the activities that we do often in a day is decision-making. And given the numerous biases that come in the way, making small improvements in our decision making process can significantly improve our capabilities to make better decisions. Below is a list of resources that will have you do that.

Personal Development

We all know that role that patience plays in investing, or in any long tenured activity. However, not all of us are born patient. Some of us like activity and cannot sit idle. How then do we play long tenured games? This post provides a possible solution what the author calls Functional Patience. While we may not be patient generally, we can learn to develop patience for certain functions.

This is an interesting meditation on the subject of 'Awe' - that feeling of over-whelm, admiration, inspiration etc. Regular and small doses of awe are important for our well-being (and IMHO creative thinking). And while we usually associate awe with grand things, like, well, the Grand Canyon, we can find it in smaller, routine things like nature, music, art etc. The article expands on this further, and lists 10 ways in which we can increase awe in our lives. [h/t to Sean for sharing this]

Blast From The Past

Revisiting articles from a past issue for the benefits of refreshing memory and spaced repetition, as well as for a fresh perspective. Below are articles from #66:

Here is an interesting perspective from the house of Chuck Acre (emphasis mine):

You are given the choice between two sums of money: one million dollars or a penny that will double every day for 30 days. Which should you choose?

Here are a couple hints. The penny that doubles daily would be worth $1.28 after the first week. After the second week, it would be worth $163.84.

You will probably reason that the penny would be worth more than the one million dollars. (Why, otherwise, all the theatrics?) By just how much, though, might surprise you.

It turns out that after doubling 30 times, the penny would be worth $10,737,418.24!

This is a terrific exercise because it highlights the not-so-obvious power of compound returns (in this case, the penny compounds at 100% for 30 periods).

I say not-so-obvious because you would have been better off taking the one million dollars until the 27th day.But in those final four days, the value of the penny increases from less than $700,000 to more than $10.7 million. Patience and a long-term perspective are required to give the power of compounding an opportunity to do its magic.

To put this in to Indian perspective, here is a chart that I think about often:

Chart courtesy of Tijori Finance

🔥 A transcript of speech delivered by an insurance executive in 1940, this is a wonderful meditation on why some people succeed over others. It serves as a wonderful guide for anyone that seeks success (don't we all?). And unlike most articles that will tell you what successful people do differently, this article goes a step further in explaining how they are able to do this differently, and therefore how you can adopt the same strategy in your pursuits. The clarity in the article, coming from almost 8 decades ago, makes this a very worth read.

Readworthy Passage

Let's read together a random, but read-worthy, passage from a randomly picked book.

When using multiples to value companies, we generally lack a sense of what comprises a high or a low value with that multiple. To get this perspective, start with the summary statistics—the average and standard deviation for that multiple. Table 4.1 summarizes key statistics for three widely used multiples in January 2010.

Since the lowest value for any of these multiples is zero and the highest can be huge, the distributions for these multiples are skewed towards the positive values, as evidenced by the distribution of PE ratios of U.S. companies in January 2010, as shown in Figure 4.1.

The key lesson from this distribution should be that using the average as a comparison measure can be dangerous with any multiple. It makes far more sense to focus on the median. The median PE ratio in January 2010 was about 14.92, well below the average PE of 29.57 reported in Table 4.1, and this is true for all multiples. A stock that trades at 18 times earnings in January 2010 is not cheap, even though it trades at less than the average. To prevent outliers from skewing numbers, data reporting services that compute and report average values for multiples either throw out outliers when computing the averages or constrain the multiples to be less than or equal to a fixed number. The consequence is that averages reported by two services for the same sector or the market will almost never match up because they deal with outliers differently.

With every multiple, there are firms for which the multiple cannot be computed. Consider again the PE ratio. When the earnings per share are negative, the price/earnings ratio for a firm is not meaningful and is usually not reported. When looking at the average price/earnings ratio across a group of firms, the firms with negative earnings will all drop out of the sample because the price/earnings ratio cannot be computed. Why should this matter when the sample is large? The fact that the firms that are taken out of the sample are the firms losing money implies that the average PE ratio for the group will be biased because of the elimination of these firms. As a general rule, you should be skeptical about any multiple that results in a significant reduction in the number of firms being analyzed.

Finally, multiples change over time for the entire market and for individual sectors. To provide a measure of how much multiples can change over time, Table 4.2 reports the average and median PE ratios for U.S. stocks from 2000 to 2010. A stock with a PE of 15 would have been cheap in 2008, expensive in 2009, and fairly priced in 2010. In the last column, we note the percentage of firms in the overall sample for which we were able to compute PE ratios. Note that more than half of all U.S. firms had negative earnings in 2010, reflecting the economic slowdown in 2009. Why do multiples change over time? Some of the change can be attributed to fundamentals. As interest rates and economic growth shift over time, the pricing of stocks will change to reflect these shifts; lower interest rates, for instance, played a key role in the rise of PE ratios through the 1990s. Some of the change, though, comes from changes in market perception of risk. As investors become more risk averse, which tends to happen during recessions, multiples paid for stocks will decrease. From a practical standpoint, what are the consequences? The first is that comparisons of multiples across time are fraught with danger. For instance, the common practice of branding a market to be under or overvalued based upon comparing the PE ratio today to past PE ratios will lead to misleading judgments when interest rates are higher or lower than historical norms. The second is that relative valuations have short shelf lives. A stock may look cheap relative to comparable companies today, but that assessment can shift dramatically over the next few months.

- From THE LITTLE BOOK OF VALUATION by Aswath Damodaran

Quotable Quotes

“Dikhayee kam diya karte hain, buniyaad ke patthar;

Zameen me dab gaye jo, imaarat unhi par kayam hai.”

[The stones in the foundation remain unseen;

But on those buried foundations flourish the monuments seen.]

Found this quote in a book that I was browsing. [h/t to Anand Tandon]

On a related note:

"What appears to be a rapid shift is often preceded by a gradual process. Our results gradually explode or vanish thanks to the small habits we repeat each day.

What radical change are you slowly marching toward? An incremental explosion or an incremental vanishing?"

- James Clear

What unseen foundations are you building today?

A Little Something Extra

Your armor is preventing you from growing into your gifts.

I’m not screwing around. All of this pretending and performing—these coping mechanisms that you’ve developed to protect yourself from feeling inadequate and getting hurt—has to go. Your armor is preventing you from growing into your gifts. I understand that you needed these protections when you were small. I understand that you believed your armor could help you secure all of the things you needed to feel worthy and lovable, but you’re still searching and you’re more lost than ever. Time is growing short. There are unexplored adventures ahead of you. You can’t live the rest of your life worried about what other people think. You were born worthy of love and belonging. Courage and daring are coursing through your veins. You were made to live and love with your whole heart. It’s time to show up and be seen.

But chlorophyll, which is yet to be fully understood, is not the only pigment in trees. Throughout a leaf’s life, four primary pigments course through its cells: the green of chlorophyll, but also the yellow of xanthophyll, the orange of carotenoids, and the reds and purples of anthocyanins.

In spring and summer, when the days grow long and bright, chlorophyll saturates leaves as the tree busies itself converting photons into the sweetness of new growth.

As daylight begins fading in autumn and the air cools, deciduous trees prepare for wintering and stop making food — an energy expenditure too metabolically expensive in the dearth of sunlight. Enzymes begin breaking down the decommissioned chlorophyll, allowing the other pigments that had been there invisibly all along to come aflame. And because we humans so readily see in trees metaphors for our emotional lives, how can this not be a living reminder that every loss reveals what we are made of — an affirmation of the value of a breakdown?

...

Two centuries after the discovery of chlorophyll, a new generation of scientists armed with a new arsenal of tools unimaginable in 1817, in that abiding way science has of only revealing new layers of reality when it lets go of its assumptions, placed bananas in various stages of ripeness under UV light and discovered that as the world’s favorite yellow fruit ripens and its chlorophyll breaks down, it not only reveals the xanthophyll of yellow, but produces the chlorophyll catabolite hmFCC — a previously unknown blue fluorescent compound.

Subsequent research has found signs of this blue pigment in devil’s ivy — the evergreen golden pothos thriving in the corner of my library in Brooklyn at this very moment — rendering the mystery of chlorophyll ongoing and filling the human heart with exhilaration. How thrilling to think that something we discovered two centuries ago, something nature created more than a billion years ago when the first green plants evolved from prokaryotes, can still shimmer with mystery — a molecular microcosm of the ultimate thrill: the knowledge that however much we might uncover, nature will never cease to be filled with surprise ripe for the reaping. And how humbling to think that we too are animals doing their best to make sense of the world with their creaturely limitations — animals whose vision evolved to peak in so narrow a band of the spectrum, in the tiny wavelength range between red and violet, blind to everything between radio and cosmic rays, blind to ultraviolet light. But if we were butterflies or reindeer, bees or sockeye salmon, bananas might be blue.

* * *

That's it for this weekend folks.

Have a wonderful week ahead!!

- Tejas Gutka

[Oct 22, 2022]

The last excerpt is beautiful. Thanks for sharing