[The Weekend Bulletin] #46: Great Companies and Great Investments

In this issue: How to find great companies; why great companies do not turn into great investments; some rituals to improve focus during WFH, advice to the investor in you; why initial corpus matters.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

If you belong to the Phil Fisher/Warren Buffet/Charlie Munger school of investing, then finding great businesses to invest in is your ultimate gospel. A lot is written about the characteristics of these great companies - they have a long growth runway, a strong competitive positioning, a skilled+visionary+honest management, an above average return on capital invested, etc.

Despite such writings being available for over six decades (Common Stocks and Uncommon Profits, tellingly the first works on investing in quality growth franchises was first published in 1958) and great advancement in data mining and analytical technologies, identifying great companies early still remains a skilful challenge. More importantly, even as one would identify great businesses, converting them into great investments is even more difficult.

To my mind, one of the greatest barriers to outstanding investments are shortening investment horizons. Nothing great is achieved in a few quarters or even a year, or two - horizons which are typically considered long term these days. Even the best of managements have taken more a few years to show results.

Investment horizons apart, there are other factors that make identifying and investing in great companies difficult. This issue attempts to look at both sides of the issue:

how to identify great businesses, and

why great businesses do not turn into great investments.

Section 1: Investing Wisdom

In last week’s issue, we looked at Henrik Bessembinder’s research around the performance of tech companies. He followed up that paper with an even more interesting one. For this paper, he looked at some so of the best and worst performing stocks over a decade (in terms of percentage returns as well as absolute wealth created) and tried to identify factors that separate the good ones from the not so good ones. As far as research papers go, this one is really simple to read, not very lengthy, and tabulates the findings for easy reference. I would therefore encourage you to read the whole paper here, or you can read a short article around it here.

As to why great businesses do not always turn into great investments, there are two issues that Henrik’s research identifies.

The first is that while the certain common characteristics are indeed observed in well performing stocks over a decade, these characteristics are more backward looking than forward. In order to study the predictive power of some of these characteristics, Henrik studies the characteristics of these firms in the decade prior to them being high return firms. He then compared them with the not-so-well-performing firms, and found that:

It can be observed that firms with the highest annualized shareholder returns in a given decade are often broadly similar to those that appear in the “Non-200” list in terms of average prior-decade characteristics. In particular, the firms that go on to deliver Top-200 returns in the following decade are, on average, within ten percent of “Non-200” firms in terms of growth in total assets, organic asset growth, as well as growth in current, fixed, and other assets, asset turnover, debt-to-asset ratio, and market-to-book equity ratio at the end of the prior decade…

…While the observable characteristics studied here had statistically significant forecast power for extreme positive and negative decade-horizon returns between 1960 and 2019, more than 98% of the variation in outcomes remains unexplained. The key open question is what portion of the unexplained variation can in principle be predicted by other (perhaps subjectively assessed) characteristics such as management quality, and what portion is purely random and therefore will prove impossible to predict?

You can read the paper here

The second issue is what Henrik started this series of papers with. His research found that the best performing firms also had large draw-downs during short periods, both during the decade of their performance and the prior decade. Investors in great businesses thus not only need a long investment horizon, but also need to stomach sharp drawdown in shorter periods. His research can be found here. You can also read it in an article form here.

Moving from first principles to second order thinking, there is a fine line that differentiates a good business from a great one. If 10% of all businesses are good, then the greats ones are probably just 1%. This article talks about what makes a company great, and why good is not good enough.

On similar lines is this article from the archives. One of the most important factors in determining long term outperformance of a business is its moat or competitive advantage. While we usually use some form of financial metric to determine the existence of such a moat, like high profit margins, market share, or returns on capital, those metrics are backward looking. They tell you that a moat exists. However, what matters for future performance is that the moat either sustains, or increases in the future. Thus, it is important that investors differentiate between a legacy moat, and reinvestment one.

Driving the point of legacy moats further, is Mark Walker of Tollymore Investment Partners in this interview on finding great stocks. He also reiterates Henrik’s findings that moats are often difficult to identify pre-mortem, and that past business performance need not sustain in the future. Some of his best investments, he says, are in businesses that were written off by investors as low moat businesses.

So if I look at the contributors to Tollymore's results and the detractors from Tollymore's results, the major contributors are from businesses which at first sight are written off as low quality businesses and that is due to usually a faulty heuristic and an inability or unwillingness to interrogate the business quality from first principles.

So for example you know investors have written off you know Tropanion as an insurance company with a heuristic associated with insurance companies that they are capital intensive strategy, mature businesses with limited opportunities to internally redeploy capital and constrained addressable markets. And I think that that heuristic has led to a really outsized investment opportunity and really if you think about the components of that company's value chain and how they cumulatively manifest in this really phenomenal business then you can kind of avoid that heuristic.

Likewise you know one of our largest holding Gym group is an old economy operationally geared financially leveraged business selling discretionary services with very high churn in a world which is enamored with high multiple of sales SAAS companies and big tech. And so if you succumb to being a victim of this sort of potential bubble and buzzwords by becoming overly enamored with these labels, if you're not interrogating from first principles what a good business is and what a poor business is.

So those types of opportunity have contributed strongly. Then what we've done badly in two main areas:

one is where we've identified obvious excellence and we've become enamored by this beautiful you know financial history going back 10/20/30 years of extraordinary consistent super normal profit generation;

and the second area is in what's often called legacy-moat type companies.

Section 2: Mental Models & Behavioral Biases

This is another one from the archives, and also shameless self-promotion. Reading the articles above reminded me of a newsletter that I had written to the clients of my pervious workplace. It was titled ‘The Painful Multibagger’, and it talks about the demons that an investor has to fight in order to realise a return that is multi-fold his investment capital. I thought it was befitting the discussion here and I hope you find it useful. Would love to hear any feedback that you may have.

Section 3: Personal Development

Work from home seems to staying around, at least for some more time. It is clearly neither as much fun or as productive as we all thought when we worked out of office. While we thought that a lot of time was eaten away in office by water cooler chats, meetings, and travel, we now realise that it isn’t easy to focus on work at home as well, especially with everyone being at home. Another issue is that of being contained within the four walls of the house, making it difficult to put start and end times to our work schedules. Here is some help in the form of seven essential rituals that you can follow to find more focus and do more work in less time.

There are a lot of messages in this very short write-up. You could use the advice in many ways. However, since we touched upon volatility a little earlier, I would like to think of this as an advice to the investor in you: We all know that volatility is inevitable in the markets. In fact, as we read above, all of the great investments tend to be very volatile in the short term. It is therefore imperative that we build acceptance for such volatility. We may not like it, but we cannot run away from it; when it comes knocking, let it find you home ready with your arsenal.

Section 4: Trivia

Here is what I asked you to think about last week:

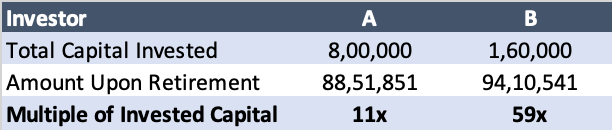

Investor A: saves INR 20,000 per year from age 26-65

Investor B: saves INR 20,000 per year from 19-26, after that never saves a penny until retirement but also doesn’t touch his savings.

Both retire at age 65, and earn a 10% return on their savings until then.

Who do you think (intuitively, without calculating) will retire with a bigger corpus, Investor A or Investor B?

The following chart traces the investments of the two investors, leaving us with some valuable lessons:

It may come as a surprise that investor A, despite saving for a longer time (all else being equal), ended up with a corpus lower than that of Investor B.

Further, while the difference in the retirement corpus may not seem to be very large, it needs to seem in the context of the amount invested:

That’s an important lesson there that investors often ignore. The value of ‘PV' and ’n' in the compounded return equation [FV=PV*(1+r)^n] has a lot of significance (something that we read about in issue 42). And therefore an unduly importance only to ‘r’ is unwarranted.

As a corollary, the above also tells us why networth on its own is not a measure of wealth created, something we read about in issue 39.

Here is the original inspiration behind the above.

* * *

That's it for this weekend folks. I hope you enjoyed this issue; let me know your thoughts/feedbacks by commenting below.

Have a wonderful week ahead!!

- Tejas Gutka

[Oct 03, 2020]

P.S.

If you come across an interesting article that you feel is insightful and worth sharing with the community of readers of The Weekend Bulletin, please email a link of the article along with a short summary/note on why you like the article to: share2TWB[at]gmail[dot]com.