A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

A small request before we get to business:

Someone whose opinion I regard highly recently mentioned that the issues are getting rather long, and that it may be worthwhile to consider sharing lesser number of links. Therefore, I thought of running a quick poll to ask you, dear reader, if you'd like me to reduce the content of the issue. You can simply vote by clicking on one of the two buttons below - it'll take only a few seconds:

The shortcomings of various valuation methodologies are well known and widely discussed. However, there is one short-coming that, to my mind, is usually under-discussed.

This is just one of many 'upsides' that valuations cannot capture. More broadly, these 'upsides' can be termed as 'Optionality' and can be grouped into a few different categories. This memo from Shawspring Partners provides the details with examples. The following is an additional demonstration of the power of Optionality:

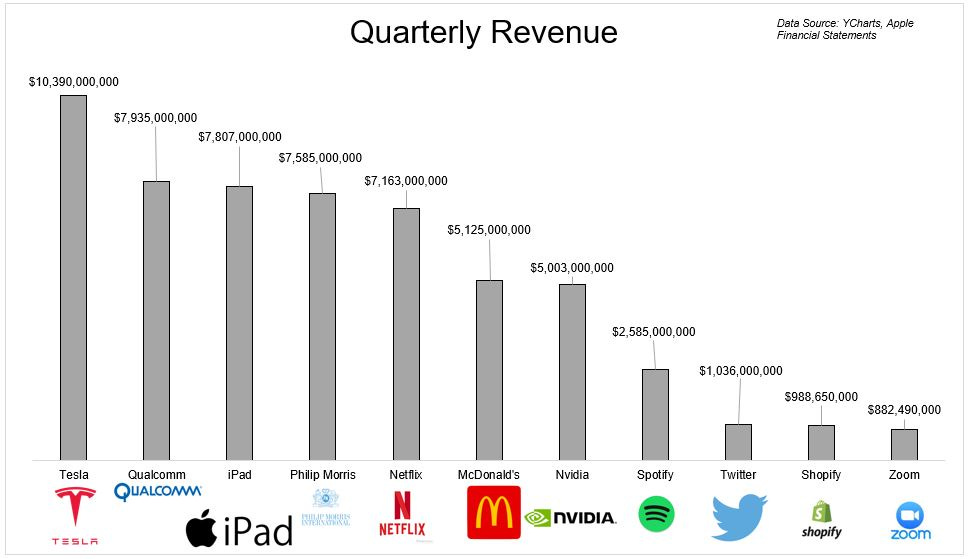

The iPad, which is the smallest of Apple’s five segments, made more revenue last quarter than Netflix or McDonald’s. It did more than the combined revenue of Spotify, Twitter, Shopify, and Zoom!! - Talk about OPTIONALITY!!

Bill Nygren's (Oakmark Funds) latest quarterly commentary touches upon an aspect that we looked at in issue 12 (balancing opposing forces). It also talks about the Dunning-Kruger effect and why investors need to be vary of it. Strong Convictions, Loosely Held!

Consider this:

He averaged 23% a year at Contrafund, vs. 12% for the S&P 500. He stormed ahead of the index again as manager of the Growth & Income Fund. He was chosen as a worthy successor of famed invested Peter Lynch at Fidelity. He'd beaten the S&P 500 consistently for nearly eight years.

Later, his hedge fund made 95% in 1997, 59% in 1998 and 38% in the first nine months of 1999 - trouncing the S&P 500, as well as hedge fund giants like Julian Robertson and George Soros.

You’d think that such track-record would have made this fund manager a celebrity. You’d be disheartened to know that his reputation was tarnished while at Fidelity, leading to him resigning. He later started his hedge fund that he managed privately, and delivered returns that not only helped him regain his reputation, but made him a star.

This is an incredible story of Jeff Vinik, successor of Peter Lynch with an almost contrary investment style.

Three take-aways from this story:

There are more than one ways to make money - pick an investment style that suits your temperament.

Your investment vehicle should match your investment style (or vice verse) - A Fund Manager’s Time Horizon is the Shortest Common Denominator ( Refer to last link in this section of Issue 47)

No matter how good someone is, achievements don’t come by easily. Success is seldom linear. Build a capacity to endure.

I usually share content that I think is timeless, rather than fleeting (stuff that is only useful currently). However, every once in a while, I make an exception to share something that is more current rather than long lasting. More often than not, these links make through into an issue either because I feel that the article is really well thought, or it provide a lot of useful data. Either way, it gives you some fodder for thought (rather than make a prediction of the near future). The latest Absolute Return Letter is one such, in my humble opinion. It talks about inflation - a hot topic in the investment world these days.

Section 2: Mental Models & Behavioral Biases

This would ideally fit in the Personal Development section. However, it is such a powerful concept, that I thought it befitting to present it here. We've all -at some point - worked for/with someone that worships busy-ness, and mistakes it for efficiency. These people think that anyone not working all the time, is wasting some time. This thinking, however, is flawed. 'Efficiency is the Enemy', claims this article. Loved this quote from the article:

...imagine one of those puzzle games consisting of eight numbered tiles in a box, with one empty space so you can slide them around one at a time. The objective is to shuffle the tiles into numerical order. That empty space is the equivalent of slack. If you remove it, the game is technically more efficient, but “something else is lost. Without the open space, there is no further possibility of moving tiles at all. The layout is optimal as it is, but if time proves otherwise, there is no way to change it.”

Section 3: Lessons From History

Drawing anecdotes from a number of books, this article provides an overview of the Japanese bubble during the 1980s. It is only by looking at history can we truly appreciate the madness of the crowds. And as Bill Nygren reminded us above, don't hold a lot of confidence in your ability in not being part of anything similar. History is proof that only context changes, our behaviour rarely does. We have, and will continue, to fall at the feet of greed as well as fear.

Section 4: Personal Development

Life seldom goes as per plan. It is, by design, random. Sometimes outcomes are rather easy to achieve, while at other times, even the best efforts may not yield desired results. Other times, it is not life, but our feelings that make some experiences less pleasurable that we initially thought them to be. One way or another, we all go through a 'Dip' in life - that time when we feel like nothing is working out, and want to quit. General advice would be to stay the course (endure, Master Wayne...), although that may not be the best solution possible. Seth Godin's book, 'The Dip' teaches you when it's okay to quit and when it's in your best interest to stick with things. This short summary outlines the key points.

If you are experiencing a Dip currently in life, and are looking for some motivation, then I would encourage you to read this story of courage and valour. This is the story of a man who set out to run a-marathon-a-day to cover 5,000 miles across Canada, with one artificial leg. All this to raise money for cancer research!! This will be one of the best stories that you'd read this weekend.

Section 5: Blast From The Past

We consume a lot interesting text in our quest for knowledge. However, with each new byte of data that we feed into our memory, we lose some bit of old information that was held. Even without the addition of new information, our memory regularly cleans our information that is held deep and not often retrieved. It is for this reason that re-reading old texts (books/articles/notes) is highly recommended.

There are other advantages to re-reading. Spaced repetition for one - when we revisit some old material, it is etched better into our long term memory. More importantly, as we gain more experiences in life, re-reading an old text can provide some fresh perspectives that we may have missed while reading earlier.

Extract From the book Richer, Wiser, Happier: How the World's Greatest Investors Win in Markets and Life. (Source: Clark Square Capital) | (Separately, welcome Paul Lountzis to the list. It's an honour to have you here).

It is to reap these benefits that this section revisits a select few articles from an earlier issue.

The deepest insights sometimes reside in the simplest observations. In a rare (no pun intended!!) public presentation, Utpal Sheth (CEO of Rare Enterprises), delivers some deep insights for investors from simple observations. He observes that there are a few mega-trends that are underway at any point in time that transcend decades, geographies, and governments. Within these mega-trends, there are a few businesses that take a large share of value (market share, profits, or cash flows). Investors that can identify such mega-trends and the leaders within those trends tend to enjoy decadal out-performance.

(This article was featured in the second issue of TWB. You can read the whole issue here).

"Having money is good - it “solves your money problems.” But without time, that money means nothing. Putting a value on time is difficult since we don’t know how much remains. And our perception of time gets warped. Fresh out of college I believed I had all the time in the world. There seemed to be an endless ocean of tomorrows to do the things I wanted.

Now I feel restless and behind the curve. As we lapsed the outbreak of COVID I felt an onset of panic. All the lockdown weeks seemed to blend together. A year has passed? Where did it all go?"

@SoumilZaveri @permanentcap DCFs cannot capture the ability of a management to redeploy cash flows into ROIC accretive lines of business that are adjacent to the current business.

@SoumilZaveri @permanentcap DCFs cannot capture the ability of a management to redeploy cash flows into ROIC accretive lines of business that are adjacent to the current business.