[The Weekend Bulletin] #65: Finding Investments, Selling Winners, Stan Druckenmiller's Biggest Mistakes,...

...Seth Klarman's Investment Style, Taming Mr. Market, On Effort and Finishing What You Start, and More.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

Section 1: Investing Wisdom

A few years back, a friend called me asking for advice (he held this misconception that people working in the stock market are smart and have all the answers). One of his investments had done exceptionally well and as a result made up nearly half of his portfolio. He was worried that such a large allocation to a single business was risky. On the other hand, the expectations that the business as well as the stock would do well over the long term held him back from selling the holding. Thus, he reached out seeking for some solution to his dilemma. What would you have advised him?

The answer to his dilemma was (and is) not as straightforward as it seems. On the one hand, we've all read about diversification and how we should not have all (or majority) of our eggs in one basket. On the other hand, we've also read about how you should not sell your winners (don't trim the flowers and water the weed, as Peter Lynch famously said).

A situation like this needs careful consideration, something that the following two articles attempt to help us with:

This article sides with Peter Lynch and provides a mathematical reasoning for letting you winners run into a becoming a larger share of your portfolio.

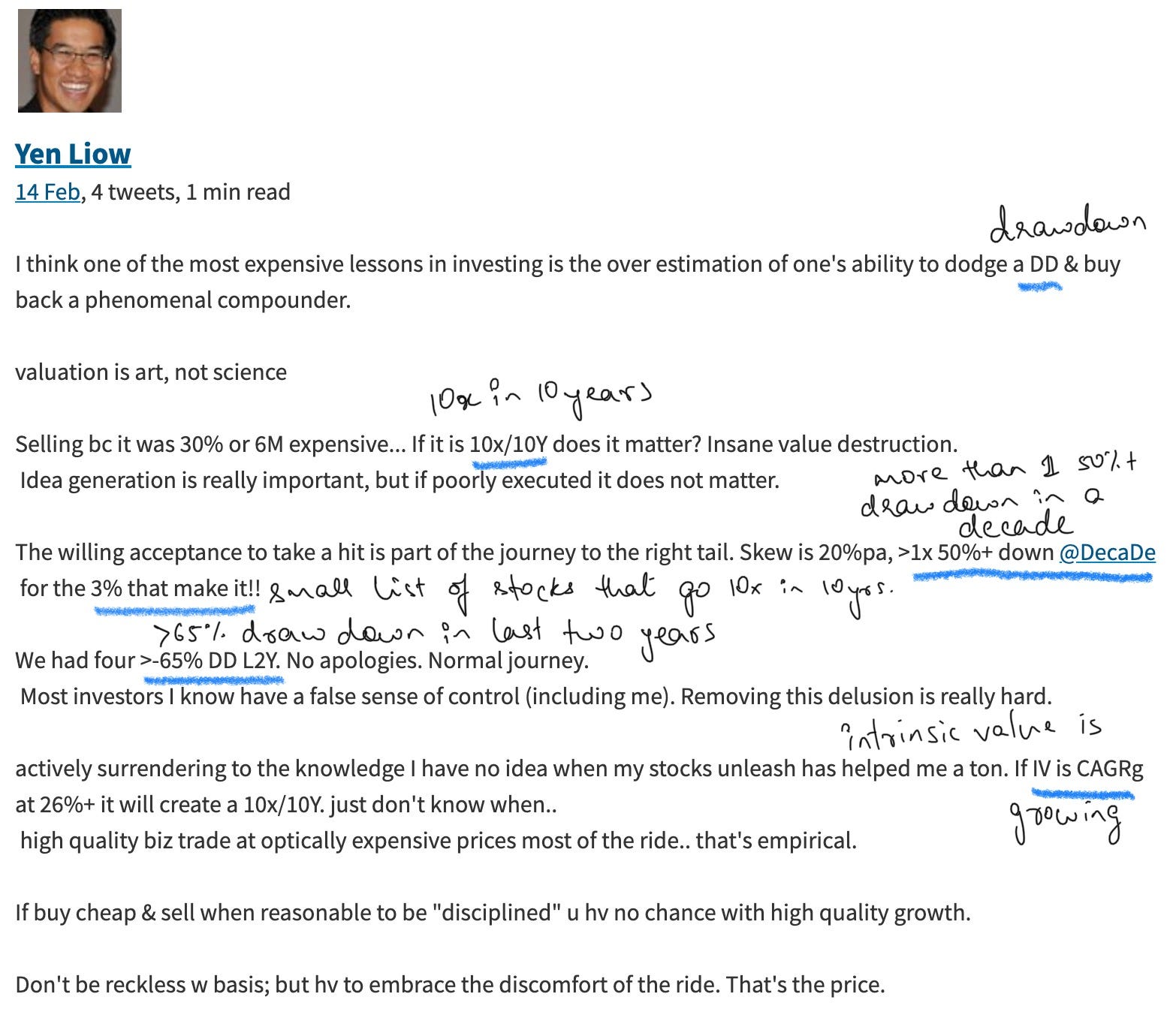

Investor Yen Liow (of Aravt Global - we met him in Issue #43) also supports the above in his own way (annotations are mine):

Taking the other side of the argument is this anecdote from the diary of an advisor. It argues that for some people, maximising returns may not be the objective, rather, they'd be much better off having some peace of mind to continue with their pursuits while their investments work for them in the background.

Both these articles make a fairly good case towards and against selling your winners. Recollecting the second of the Three Laws of Human Behaviour from last week, behaviour is a function of the person, and their environment. Thus, the answer to this dilemma of 'to sell or not to sell' also depends on you and your circumstances. There is no one-size-fits-all answer to this, as with most things in investing.

Upon reading about my friend above, some of you may wonder that the question of selling is secondary. The primary question is, how does one go about finding such successful investment ideas? Well, Issue 48: Ingredients of Long Term Value was dedicated to this subject. However, for those looking at more specific answers, this newsletter (worth a follow) does a nifty job of curating the ideation process of some well regarded investors. You'll find that each investor had his own unique ways to ideate; there is no one-size-fits-all answer to this, as we saw earlier.

Let us now shift focus from a list of investors to one specific investor. This article is a nifty little write up on Seth Klarman, the investor and his investing style. It details the various perspectives laid out by Seth on valuing a business, including notes from his book. Think of this as a crash course into Seth's investing process.

Lastly, if you are young investor, or someone about to start, Chris Cerrone of Akre Capital has some helpful advice for you here.

Section 2: Mental Models & Behavioral Biases

Sometimes, the shortest of write-ups carry the weight of a book. This little anecdote about Stan Druckenmiller is one such. In about 10 tweets, it tells us that behavioural biases spare no one, not even the best of us. Understanding and being aware of our psychological shortcomings is one thing, but dealing with them real-time is another. Adding a little bit of friction or delaying taking action can save us at times, while at other times, it's best to just know that mistakes are a part of the process and move on.

We've all read about Mr. Market and his manic-depressive behaviour as defined by Ben Graham and espoused by many over the years (Market fluctuations can draw you into doing something that works against your best interests. It’s best to ignore it most days.). However, not a lot is written about how best can one ignore Mr. Market's offers. This article has a few suggestions - three, to be specific.

Section 3: Lessons From History

This is a very interesting write-up urging us to not draw the wrong lessons from the dot-com bubble and crash. It argues against the notion that the dot com bubble was a result of investors over-estimating the internet. In fact the author believes that investors under-estimated the internet back then. Further, it also argues that while you may notice a speculative bubble in the market, that is not reason to exit the market, as was also the case during the dot com bubble. Read on to find out what lessons should we really be drawing, if not the aforementioned (worth reading this one as it has implications for the current market conditions).

Section 4: Personal Development

A good meditation on the value of effort, this article makes a case for being interested in the process rather than the outcome. Most people would like to lose weight, but don't want to exercise, or most people would like to have a book written, but don't want to write the book. It argues that best things happen when we love the process, the pain and the grind that comes with it, and not just the end-result.

Consider the following:

Aren't we all like the protagonist here, with too much to do and too little time? Don't we all have a volume of ideas but not enough time to work on any of them? Is there a way that we can be more productive with at least some of our ideas? Can we enjoy some of those figs before they go dead? The following framework exhibits one of the ways in which we can do this:

This article explains the above in details.

Quotable Quote

* * *

That's it for this weekend folks.

If you enjoyed reading this issue → please hit the like button

If you have any feedback/interesting articles that you’d like to share → simply reply to this email/leave a comment below.

Have a wonderful week ahead!!

- Tejas Gutka

[Mar 06, 2021]