[The Weekend Bulletin] #98: Absence of Risk ≠ No risk; Setting Expectations;...

...Patient Capital, 100 baggers, Managing Oneself, and more.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

🪔🧨 Season's Greetings to everyone from the Indian Subcontinent. 🧨🪔

May the festival of lights bestow upon you inner illumination, self-actualisation, and eternal bliss. May the New Year be a healthy, peaceful, and insightful one.

Section 1: Investing Wisdom

This white-paper by AQR talks about the need to set investor expectations down after a stupendous run-up in the markets. It also provides an interesting perspective on diversifying risk (rather than assets). The paper will be a good read for the sake of your financial well-being.

"Expected returns across a range of asset classes today are lower than their historical averages, yet the same is not true for expected risks. The past decade presented overall very friendly conditions for stocks and bonds (generally growth above forecasts, inflation below, and falling yields), but it would be imprudent to assume these conditions will repeat themselves over the next decade. Setting expectations — for investors, boards, and other stakeholders — is arguably going to be much more important from here"

This decade old interview of Bruce Greenwald makes for an interesting read for three reasons:

it covers some basics of investing;

"Always start with the assets. Then look at the earnings power and see if it's protected by the assets. And only then, and this is what Buffett taught people to do, look to pay something for growth, because growth is only valuable if the investment in growth earns more than the cost of capital. And if it doesn't, growth can destroy value. Growth is not a valuable thing as a rule. So, and if you're going to buy that, you better be very sure of the franchise."

it makes an interesting point that the absence if risk is not no risk;

"People are predisposed to do stupid things. That when they think markets are going well, they're sure, like long-term capital management was, that risk has gone away. It's not just, by the way, in housing markets. If you look at credit default swaps on sovereign debt in 2007, Dubai sovereign debt was trading at four basis points.

That is, you could buy insurance against a default on Dubai sovereign debt for four one-hundredths of a percent. That means you were betting that there was less than a chance, if you wrote that insurance, in 2,500 years that a country like Dubai, in the most unstable region of the Earth, based on the most unstable commodity at a peak price, had a less, had a one chance in 2,500 years of defaulting."

and most importantly, it demonstrates that even the best investors can go drastically wrong for an extended period;

"I'll do the one that I've been wrong on for years. I've always thought Amazon is a bubble. They have no customer captivity. They don't have enough scale that it's hard to replicate. They occupy a really big market. They're not specialized at all.

....I've been semi-wrong about Apple, which I think is a bubble, because we have a lot of experience with consumer electronics companies."

(These statements were made in 2010!)

This interview of Bill Martin of Raging Capital Ventures explores the key ingredients of a winning investment, the early steps of a research process, the need to see beyond numbers in smallcaps and much more.

The beauty of investing is that there is room for all kind of styles and philosophies. These can range from extremely complex computational models that trade within the fraction of a second to a simple and inactive an approach as below:

He explained his technique, which was ultimate in simplicity. When during a bear market he would read in the papers that the market was down to new lows, and the experts were predicting that it was sure to drop another 200 points in the Dow, the farmer would look through a Standard & Poor’s Stock Guide and select around 30 stocks that had fallen in price below $10 – solid, profit-making, unheard-of, little companies (pecan growers, home furnishings, etc) and paid dividends. He would come to Houston and buy a $25,000 package of them.

And then, one, two, three or four years later, when the stock market was bubbling and the prophets were talking about the Dow hitting 1500, he would come to town and sell his whole package. It was as simple as that. During the subsequent years as I cultivated Mr. Womack (and hunted ducks on his rice fields) until his death, I learned much of his investing philosophy.

He equated buying stocks with buying a truckload of pigs. The lower he could buy the pigs, when the pork market was depressed, the more profit he would make when the next seller’s market would come along. He claimed that he would rather buy stocks under such conditions than pigs because pigs did not pay a dividend. You must feed pigs.

He took a “farming” approach to the stock market in general. In rice farming, there is a planting season and a harvest season; in his stock purchases and sales he strictly observed the seasons. Mr. Womack never seemed to buy a stock at its bottom or sell it at its top. He seemed happy to buy or sell in the bottom or top range of its fluctuations. He had no regard whatsoever for the old cliché – Never Send Good Money After Bad – when he was buying. For example, when the bottom fell out of the bottom in the market of 1970, he added another $25,000 to his previous bargain-price positions and made a vitual killing on the whole package.

In a nutshell: Buy when there is blood on the street, sell when there is Euphoria, and do nothing in between!! (The above excerpt is from this article)

Some other worth-while reads:

This super-thread on finding and riding 10-100 baggers

This announcement by Sequoia Capital that may well be a new turning point in the Venture Capital industry.

Section 2: Mental Models & Behavioral Biases

This is a nifty resource worth exploring. It is a collection of some important investing and life lessons (neatly categorised), that is worth bookmarking.

Section 3: Personal Development

This is probably one of the best resources that I have read so far on how the modern day knowledge worker can work around to having a meaningful working life. Titled “Managing Oneself” this article by Peter Drucker acts as a guide that anyone with modest talents can use to transform into an out-standing performer.

Here is an interesting exercise to build those habits that you have been wanting to work upon:

Source: Linkedin

Section 4: Blast From The Past

Revisiting articles from a past issue for the benefits of refreshing memory and spaced repetition, as well as for a fresh perspective. Below are articles from #26:

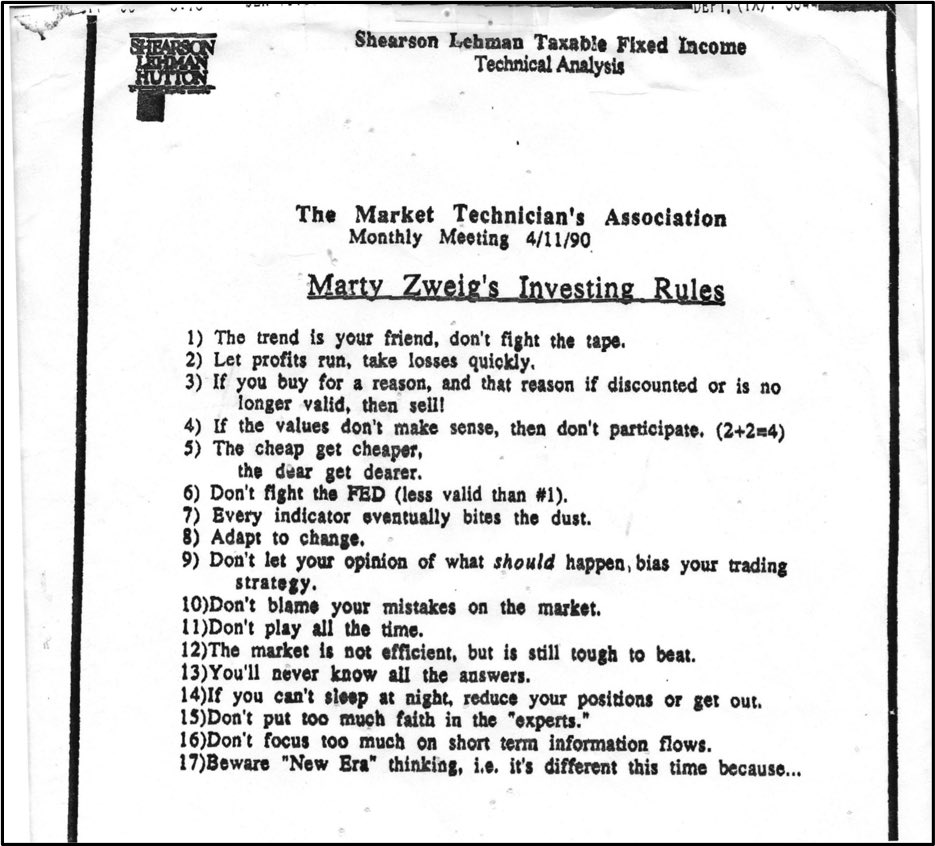

Here is a list of investing rules from the great Martin Zweig, author of the book Winning on Wall Street (also known for devising the Put/Call Ratio and the famous quote 'Don't fight the Fed').

Section 5: Readworthy Passage

Let's read together a random, but read-worthy, passage from a randomly picked book.

OUR WELL-BEING LIES IN OUR ACTIONS

“Those obsessed with glory attach their well-being to the regard of others, those who love pleasure tie it to feelings, but the one with true understanding seeks it only in their own actions. . . . Think on the character of the people one wishes to please, the possessions one means to gain, and the tactics one employs to such ends. How quickly time erases such things, and how many will yet be wiped away.”

— MARCUS AURELIUS, MEDITATIONS, 6:51, 59

If your happiness is dependent on accomplishing certain goals, what happens if fate intervenes? What if you’re snubbed? If outside events interrupt? What if you do achieve everything but find that nobody is impressed? That’s the problem with letting your happiness be determined by things you can’t control. It’s an insane risk.

If an actor focuses on the public reception to a project—whether critics like it or whether it’s a hit, they will be constantly disappointed and hurt. But if they love their performance—and put everything they have into making it the best that they’re capable of—they will always find satisfaction in their job. Like them, we should take pleasure from our actions—in taking the right actions—rather than the results that come from them.

Our ambition should not be to win, then, but to play with our full effort. Our intention is not to be thanked or recognized, but to help and to do what we think is right. Our focus is not on what happens to us but on how we respond. In this, we will always find contentment and resilience.

From THE DAILY STOIC by Ryan Holiday

Quotable Quotes

'Everything arises and passes away.'

The best short advice ever:

Marcus Aurelius on The Good Luck of Bad Luck (not exactly a quotable quote, but a thought provoking one for sure):

"Be like a headland: the waves beat against it continuously, but it stands fast and around it the boiling water dies down. “It’s my rotten luck that this has happened to me.” On the contrary, “It’s my good luck that, although this has happened to me, I still feel no distress, since I’m unbruised by the present and unconcerned about the future.” What happened could have happened to anyone, but not everyone could have carried on without letting it distress him. So why regard the incident as a piece of bad luck rather than seeing your avoidance of distress as a piece of good luck? Do you generally describe a person as unlucky when his nature worked well? Or do you count it as a malfunction of a person’s nature when it succeeds in securing the outcome it wanted?

…

So then, whenever something happens that might cause you distress, remember to rely on this principle: this is not bad luck, but bearing it valiantly is good luck."

Source: BrainPickings

* * *

That's it for this weekend folks.

Have a wonderful week ahead!!

- Tejas Gutka

[Nov 06, 2021]