[The Weekend Bulletin] #95: Forecasting Growth, Lessons from Nature, Monty Hall Problem,...

...more than Risk and Return, Investment Manual, Circle of Influence, The Need for Ravana, and more.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

Section 1: Investing Wisdom

"we are investors who happen to be in the asset management business, rather than asset managers who happen to be investors"

Modelled upon Berkshire Hathaway's Owner's Manual, this semi-annual investor letter from DMZ Partners makes for a very interesting read. It lays out the fifteen core principles that drive the investment philosophy and process at DMZ. Very rare to see such detailed elucidation of operating principles.

Investing is all about the future, and the future is unpredictable. In addition to this the general over-confidence that we have on our own ability as well as our over- optimism/pessimism about the future, makes forecasting future growth an ardent task. While there is no exact science to forecasting, the following five part series lays out a simple frame-work to reduce such forecasting errors:

FORECASTING GROWTH PART I: THE SIREN SONG OF GROWTH - we are all forecasters, whether we explicitly forecast or not. We are usually over-optimistic about the future, making forecasting error-prone.

FORECASTING GROWTH PART II: USING BASE RATES - the inside view and the outside view in forecasting.

FORECASTING GROWTH PART III: PROBLEMS WITH BASE RATES - whats good about base rates is also a problem with them.

FORECASTING GROWTH PART IV: BEYOND BASE RATES - marrying the inside view with the outside view.

FORECASTING GROWTH PART V: CATEGORY KILLERS & POSITIVE FEEDBACK LOOPS - when to ignore base rates.

Just as capital investments have evolved from tangible to intangible, so have the measurement of investment success. Traditionally, investment attributes have been quantified into measures like standard deviation (risk), alpha/beta (returns), Sharpe/Sortino Ratios (risk-adjusted returns), drawdowns (losses) etc. However, overtime a more nuanced and probably non-quantifiable understanding of these attributes has emerged. For instance, volatility is no longer considered as a risk as broadly as it was in the decades earlier. Similarly, there are aspects of investment success that are non-quantifiable but more important than their quantifiable counterparts like alpha, out-performance, raking, rating etc. This article provides a few such measures that we should all try and live by.

Morgan Housel is a master story-teller, and one of the best financial writers of our time. In his latest, he draws two lessons from nature about cycles and compounding. A very insightful read.

This short note presents some very interesting data on multi-baggers. It shows that multibaggers are not that rare - about 45% stocks increased their market values by 5x, 30% of those increased their market value by another 5x, 30% of those increased their market value by another 5x, and so on... Does this mean that multi-baggers are easy to find, or that using a momentum strategy, if you buy stocks that have increased their market value by 5x recently, you will end up multiplying your wealth at a similar rate in the future as well? The article will tell you why it isn't so easy (my favourite quote on investing: simple, but not easy).

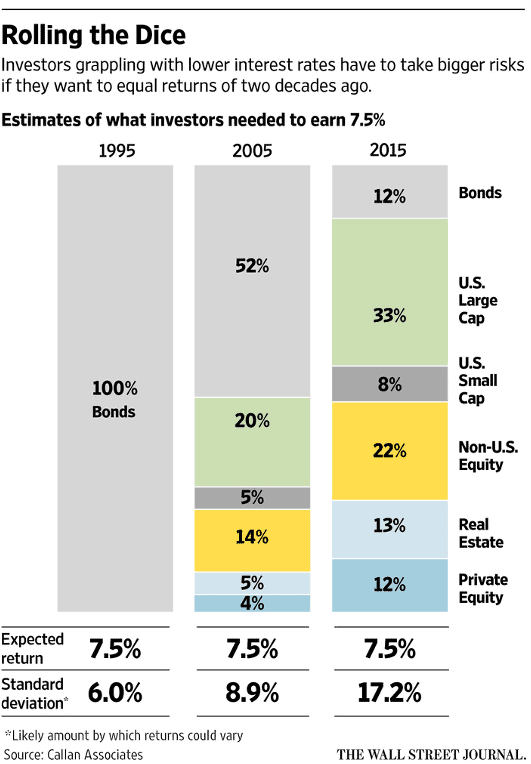

The following chart is worth pondering upon. It shows how portfolio components have had to change over the last few decades in order to simply earn the same returns. There are a few important lessons here: a) diversification is more important now than ever, b) investors have had to take a higher risk (exposure to riskier asset classes) to earn the same return over time - it is increasingly tough to make money, and c) building portfolios based on past performance may lead to sub-optimal returns.

Source: This article

Section 2: Mental Models & Behavioral Biases

Part V of the above five-part series on forecasting growth explains the concept of feedback loops - positive and negative. This is an important mental model to add to our toolbox for understanding businesses, especially in the age of technological revolution.

The importance of probabilistic thinking in investing cannot be under-stated. However, every once in a while, there comes a problem that baffles even the most learned in the subject. This one is called the Monty Hall problem, and is based on a TV game show from the 50-80's era. Here's the problem:

A contestant is faced with three doors. Behind one of them is a sleek new car. Behind the other two are goats. The contestant picks a door, say Door 1. To build suspense, Monty opens one of the other two doors, say Door 3, revealing a goat. To build the suspense still further, he gives the contestant an opportunity either to stick with their original choice or to switch to the unopened door. You are the contestant. What should you do?

On the face of it, it seems that there is an even chance (50-50) of the car being behind any door, and therefore it should not make a difference whether you switch or not. Most PHDs would agree with you, as the article explains. However, you'd still be wrong.

Regular readers will be reminded of a similar problem that was posed in #36:

There was some further discussion on this topic in the comments section.

Section 3: Personal Development

More the merrier has been a long held belief of mankind. From hunter-gatherers, we have evolved into consumers and hoarders. This belief also extends to our network of influence. With the proliferation of the internet and the advent of social media, we are constantly increasing the size of our networks. However, if experts are to be believed, when it comes to our networks, the smaller the better. This article explains why.

In the spirit of Dussehra (victory of good over evil) that was celebrated in India yesterday, here is an entrepreneur explaining Why we all need a Ravana (evil forces) in our lives.

Section 4: Blast From The Past

Revisiting articles from a past issue for the benefits of refreshing memory and spaced repetition, as well as for a fresh perspective. Below are articles from the #23 of TWB:

This slightly dated presentation sets the context of why investing is simple, but not easy. Aptly titled 'Investing is Hard' it walks you through some real life situations of companies like Apple, Valeant, Altria, Softbank etc, to demonstrate why it is so.

Unpredictability of stock price movements in not the only reason that investing is difficult. It is also difficult because MOAT - regarded as one of the more important factors in fundamental investing - is not always reliable. For, as this article highlights, seemingly infallible moats can be filled, or an altogether new fort with different moat may come up elsewhere, leading to investors completely bypassing your fort.

A little humor from history to lighten up the mood. The first totally honest stock market report ever.

Section 5: Readworthy Passage

Let's read together a random, but read-worthy, passage from a randomly picked book.

THE POWER OF COMMON KNOWLEDGE

To get these spectacular returns you had to buy and sell at exactly the right time. But even if you missed the highs or the lows, you would have done better to have invested in any of the familiar companies mentioned above than in some of the esoteric enterprises that neither of us understands.

There’s a famous story about a fireman from New England. Apparently back in the 1950s he couldn’t help noticing that a local Tambrands plant (then the company was called Tampax) was expanding at a furious pace. It occurred to him that they wouldn’t be expanding so fast unless they were prospering, and on that assumption he and his family invested $2,000. Not only that, they put in another $2,000 each year for the next five years. By 1972 the fireman was a millionaire—and he hadn’t even bought any Subaru.

Whether or not our fortunate investor asked any brokers or other experts for advice I’m not certain, but many would have told him his theory was flawed, and if he knew what was good for him, he’d stick with the blue chips the institutions were buying, or with the hot electronics issues that were popular at the time. Luckily the fireman kept his own counsel.

You might have assumed it’s the sophisticated and high-level gossip that experts hear around the Quotron machines that gives us our best investment ideas, but I get many of mine the way the fireman got his. I talk to hundreds of companies a year and spend hour after hour in heady powwows with CEOs, financial analysts, and my colleagues in the mutual-fund business, but I stumble onto the big winners in extracurricular situations, the same way you could:

Taco Bell, I was impressed with the burrito on a trip to California; La Quinta Motor Inns, somebody at the rival Holiday Inn told me about it; Volvo, my family and friends drive this car; Apple Computer, my kids had one at home and then the systems manager bought several for the office; Service Corporation International, a Fidelity electronics analyst (who had nothing to do with funeral homes, so this wasn’t his field) found on a trip to Texas; Dunkin’ Donuts, I loved the coffee; and recently the revamped Pier 1 Imports, recommended by my wife. In fact, Carolyn is one of my best sources. She’s the one who discovered L’eggs.

L’eggs is the perfect example of the power of common knowledge. It turned out to be one of the two most successful consumer products of the seventies. In the early part of that decade, before I took over Fidelity Magellan, I was working as a securities analyst at the firm. I knew the textile business from having traveled the country visiting textile plants, calculating profit margins, price/earnings ratios, and the esoterica of warps and woofs. But none of this information was as valuable as Carolyn’s. I didn’t find L’eggs in my research, she found it by going to the grocery store.

Right there in a freestanding metal rack near the checkout counter was a new display of women’s panty hose, packaged in colorful plastic eggs. The company, Hanes, was test-marketing L’eggs at several sites around the country, including suburban Boston. When Hanes interviewed hundreds of women leaving the test supermarkets and asked them if they’d just bought panty hose, a high percentage answered yes. Yet most of them couldn’t recall the name of the brand. Hanes was ecstatic. If a product becomes a best-seller without brand-name recognition, imagine how it will sell once the brand is publicized.

- From ONE UP ON WALL STREET by Peter Lynch

Quotable Quotes

* * *

That's it for this weekend folks.

Have a wonderful week ahead!!

- Tejas Gutka

[Oct 16, 2021]