[The Weekend Bulletin] #148: Seth Klarman, Michael Burry, Howard Marks, Steve Waugh,...

...Excellent vs Competent Fund Managers, Anxiety Premium, Hare and the Tortoise, Progress System, and more.

A digest of some interesting reading material from around the world-wide-web. Your weekly dose of multi-disciplinary reading.

Investing Wisdom

The general advice on the street is to avoid catching a falling knife. However, Howard Marks disagrees. In this short excerpt from a 2018 talk he explains why the refusal to catch a falling knife is a rationalization for inaction.

A good post detailing how Steve Waugh dealt with a failure, and how some of his lessons can be applied to investing. Cant skip this if you are a cricket fan.

This long post makes a distinction between stress and anxiety, and posits that the long term returns in equity comes not from volatility, but from investors managing their anxiety successfully.

This article reproduces a section of Seth Klarman's letter where the famed investor reminds us of the forgotten lessons of the 2008 financial crisis.

If you’re hard-working, intelligent and good at exams you can become a fund manager. But that won’t make you a great fund manager, claims this post. Read on to find out what differentiates excellent from competent.

Mental Models & Behavioral Biases

This short article claims that we have learnt the wrong lesson from the classic Hare and The Tortoise fable. Slow and steady wins the race under certain circumstances only.

Personal Development

The abundance of information and the distraction from notifications makes it hard to stay focused and productive. Today, more than ever, there is a need for a system to manage our days, and to stay focused on what matters. Without such a system, the time just passes, the days just blur, and we find ourselves running around like a headless chicken. While a lot has been written on this subject, this series of emails is amongst the few very detailed explanations of how to plan, manage, and review your daily, weekly, and longer affairs.

Blast From The Past

Revisiting articles from a past issue for the benefits of refreshing memory and spaced repetition, as well as for a fresh perspective. Below are articles from #73:

While pricing power is a powerful tool to identify a good business, it is but only one of the many tools that help differentiate a good business from a not so good one. The following two part twitter thread lists a number of variables that make a business good, and also provide a nifty scoring model that can be used as a screener to shortlist good businesses [Part 1; Part 2].

The following infographic summarises some of the characteristics of a good business:

A quantitative scoring model measures the results rather than the inputs. In other words, while factors like high return ratios, strong cash flow generation etc characterise a good business, these numbers are outcomes that are driven by a number of soft factors that cannot be screened for. These are aspects of the business that shape it over a long period of time (think decades). In this post, Chris Mayers - author of the book 100-baggers, discusses some such soft factors that he has observed in his research.

A lot of financial literature celebrates contrarianism. We love to hear stories of investors that took a stand against the market and eventually came out winners. While these stories make for very interesting read, and also sound inspiring, what they mask is the pain that investors suffer in taking such a stand. One of the most famous recent stories of contrarianism is that of Micheal Burry (The Big Short) who correctly predicted and profited from the 2008 housing crisis. Though he made his investors lots of money in the end, these same investors experienced excruciating losses in the short term while they waited for the housing market to collapse (some even threatened to sue). As a result, none of Burry’s investors said thank you when the dust finally settled. In order to understand the agony that an investor suffers in taking a contrarian view to the markets, I invite you to read this post that reproduces short paragraph's from Seth Klarman's letters preceding the tech bust. It is for going through this agony that Seth Klarman is the revered investor that he is. Respect!!

Readworthy Passage

Let's read together a random, but read-worthy, passage from a randomly picked book.

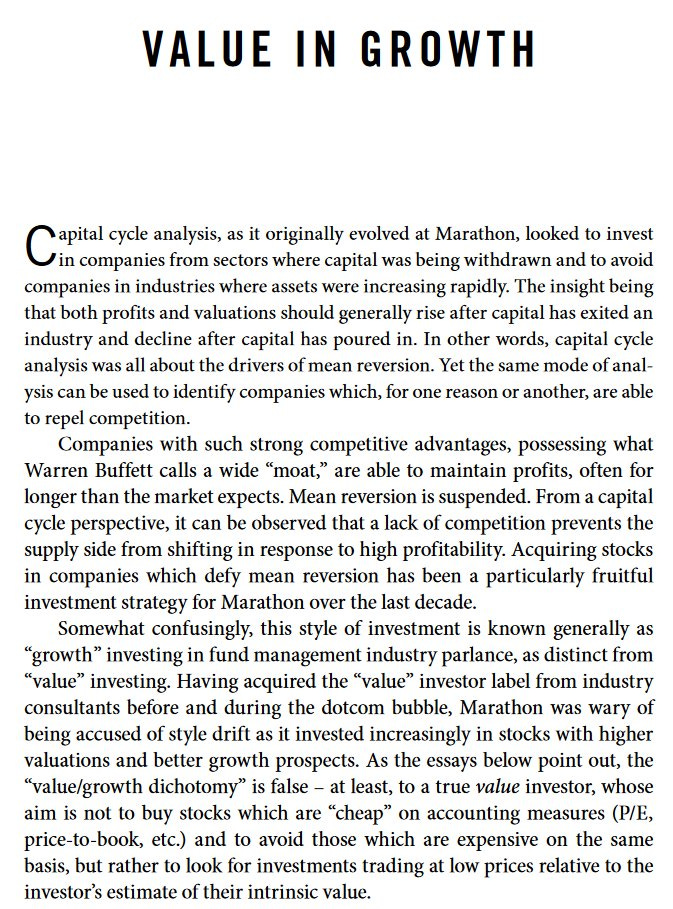

- From Capital Returns: Investing Through the Capital Cycle: A Money Manager’s Reports 2002-15 by Edward Chancellor

Quotable Quotes

“People are always asking me where the outlook is good, but that’s the wrong question. The right question is: Where is the outlook most miserable?”

"Successful value investing is not about buying companies that screen cheaply. It's about imagining a future others do not because they are blinded by fear."

* * *

That's it for this weekend folks.

Have a wonderful week ahead!!

- Tejas Gutka

[Feb 18, 2022]

We need more cricket and investing content I reckon! :P